IMF: The Global Economic Recovery Will Be Long, Uneven, and Uncertain

The International Monetary Fund (IMF) has slightly improved its forecast for the global economy. It now estimates that this year’s decline will be “only” 4.4%. At the same time, the IMF warns that the pandemic has left deep scars on the economy. The recovery will take a long time and will be accompanied by uncertainty and widening inequality.

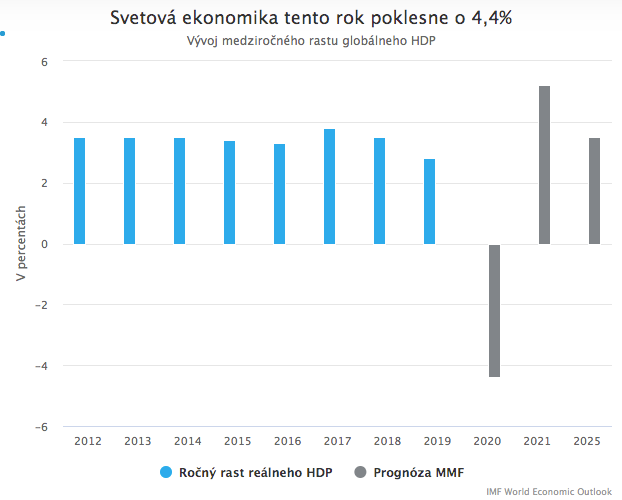

According to the IMF’s latest estimate, the global economy will contract by 4.4% this year. This is an improvement compared with the June forecast, but it is still one of the worst figures in modern history. This relative improvement is mainly due to a faster-than-expected rebound in the euro area and U.S. economies. Euro area countries improved, on average, by 1.9 percentage points compared with the June forecast, while the United States improved by as much as 3.7 points.

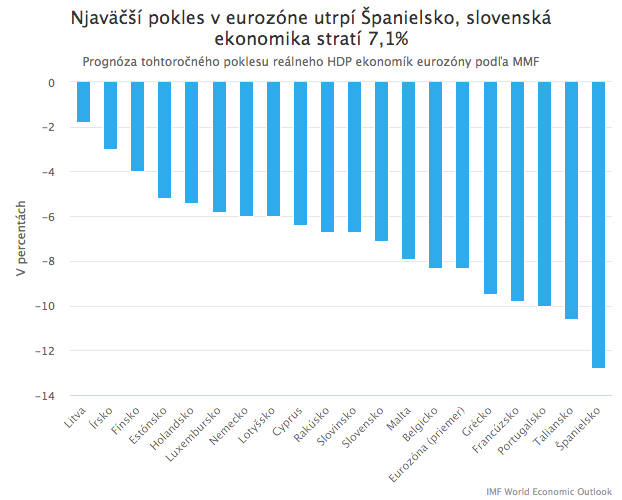

Even after the forecast upgrade, both economic blocs still face substantial declines. The U.S. economy is expected to fall by 4.3% this year, while the eurozone economies, on average, will contract by a frightening 8.3%, with the sharpest drops in southern countries such as Italy and Spain. The Slovak economy is expected to record a 7.1% decline.

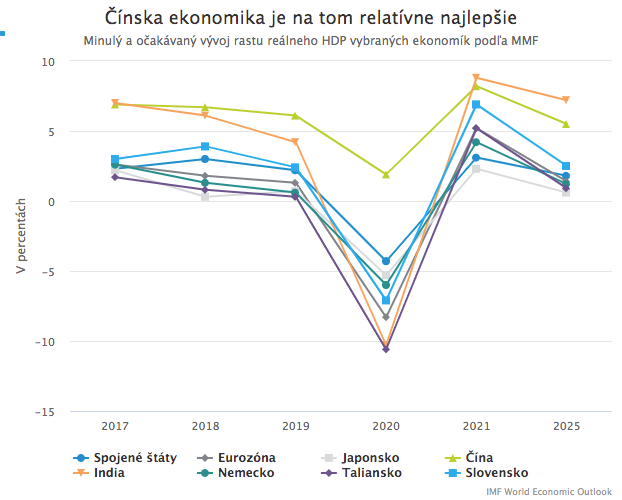

The only major global economy that is not expected to contract this year despite the raging pandemic remains China, for which the IMF forecasts 1.9% growth this year. Other Asian economies, however, are expected to fare noticeably worse, even though China’s relatively rapid recovery will also lift them somewhat. India is expected to suffer a contraction of more than 10%. Emerging markets excluding China are expected to slow by 5.7% on average.

Next year, the global economy is expected to rebound sharply by 5.2%, despite the IMF’s assumption that the pandemic will be fully brought under control only in 2022. The strongest rise in 2021, averaging 6%, is expected in emerging markets, which not only suffered steeper declines this year than advanced economies (with the exception of China) but also have higher long-term growth rates. Advanced economies will have to make do with 3.9% growth next year. Even after that rebound, their GDP will still be about 2% below pre-pandemic levels.

The crisis will leave deep scars

After the jump in 2021, average annual growth of the global economy is expected to slow to 3.5% over the medium term. The coronavirus pandemic will thus leave deep scars in the global economy that will heal only very slowly.

The pandemic is expected to reduce the potential GDP of the 10 most advanced economies by as much as 3.5% over the medium term. Their real economic growth is expected to settle at only 1.7% after 2021. In addition to the damage caused by the pandemic, long-term unfavorable demographic trends will likely contribute to this low growth pace.

Economic growth in more dynamic emerging markets is expected to settle at 4.7% over the medium term, significantly below the 5.6% average growth rate in 2000 to 2019. The pandemic is expected to shave as much as 5.5% off their potential GDP. They will be hit especially through lower commodity prices, reduced demand in advanced economies, and a long-term decline in tourism. Structural slowing in China, which began even before the pandemic, will also play a role; after a sharp jump in China’s economy in 2021, growth is expected to continue trending toward permanently lower levels.

Rising poverty and widening inequality

In addition to slowing growth for many years to come, the coronavirus crisis has brought other extremely negative consequences. In just a few months, it effectively erased more than two decades of global progress in reducing poverty. The IMF estimates that as many as 90 million people will fall below the threshold of extreme poverty due to the pandemic.

These are primarily people in developing countries who work in the informal economy, lack the safety nets present in advanced countries, and economic migrants who often support entire families back home and whose crisis eliminated their ability to travel for work.

Beyond its uneven impact across countries, the pandemic has also amplified existing inequality within advanced economies. It has hit hardest low-income people working mainly in services, as well as those working in the informal economy with limited access to state social-support programs. Conversely, it has affected least those with higher incomes working in sectors like IT or finance who can work from home and have the necessary equipment.

Current conditions also favor rising inequality at the firm level and increasing market concentration. Smaller companies with poorer access to government support, firms in low-margin sectors, and those with higher interest costs face existential problems today. By contrast, large technology companies, which already had dominant market positions even before the pandemic, are benefiting from current developments. This has been reflected in their shares, which have surged since the crisis began. Their founders and shareholders, already among the world’s richest, have seen an even steeper rise in wealth this year, while millions of people are slipping into poverty.

Moreover, the current situation creates conditions for inequality to deepen in the future. School closures and disruptions to education once again hit the most vulnerable and poorest children the hardest, those who lack equipment and suitable conditions for online learning and often face very unfavorable home environments. Especially in developing countries, school is often the only place where children have access to hygiene, healthcare, and subsidized meals. Several months of disrupted schooling can disadvantage especially younger children for life.

Another legacy of the crisis: a flood of debt

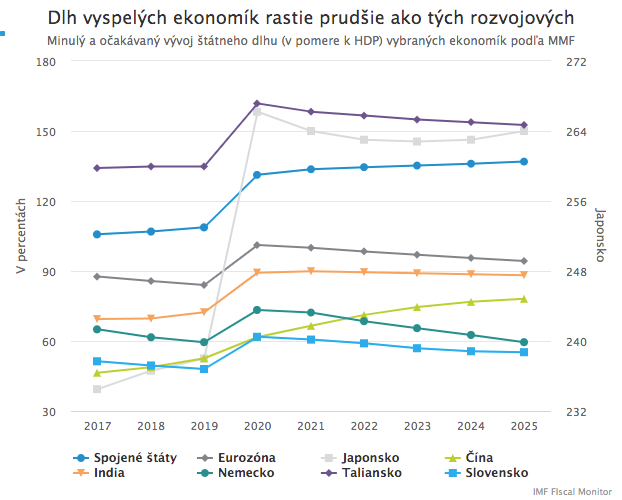

Another problematic legacy of the coronavirus crisis is a sharp rise in debt, public, corporate, and household.

Since the outbreak of the pandemic, governments have spent nearly USD 12 trillion supporting their economies, about 12% of global GDP. As the IMF emphasizes in its Fiscal Monitor, this support was absolutely necessary and helped avert the worst outcomes. The downside, of course, is a large increase in public debt.

This increase is more pronounced in advanced economies, which can afford greater debt accumulation. Since the start of the pandemic, advanced economies have provided support equivalent to as much as 9% of GDP in direct fiscal measures and another 11% of GDP through various liquidity-support measures, including central bank quantitative easing. Less developed economies could afford only about 5.5% of GDP in total support.

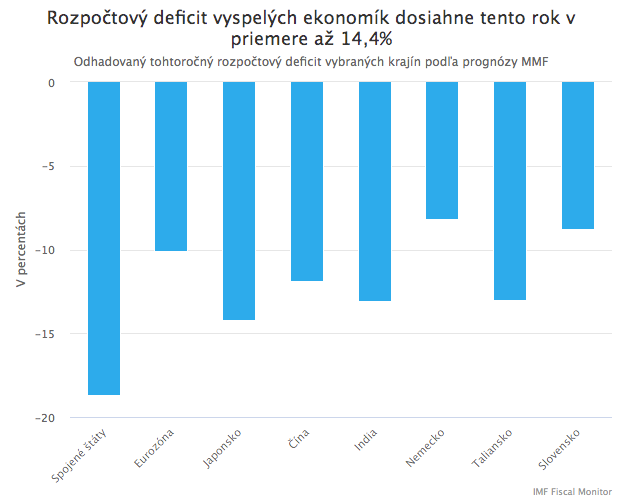

It is therefore not surprising that advanced economies are currently seeing a larger rise in debt than developing countries. Their budget deficit is expected to reach an average of 14.4% this year, while their total public-debt-to-GDP ratio is expected to rise by nearly 20 percentage points to a record 125.5%. In most advanced countries, except the United States, this ratio is expected to stabilize thereafter, helped by long-term low interest rates.

In emerging economies, the average budget deficit is expected to reach 10.7% this year, while their public-debt-to-GDP ratio is expected to rise from 52.5% last year to 62.2%. There is a risk, however, that unlike in advanced economies, it will not stabilize in the following years but will continue rising persistently.

Corporate debt has also surged, of course. This year, the bond market saw a record volume of issuance. A similar principle applies to corporate (and household) debt as to public debt: large and financially strong companies that can borrow today at record-low, often even negative, interest rates should not have trouble repaying in the future and can use such “cheap money” for productive investment. By contrast, smaller and riskier firms in weaker financial condition may face serious repayment problems in the future.

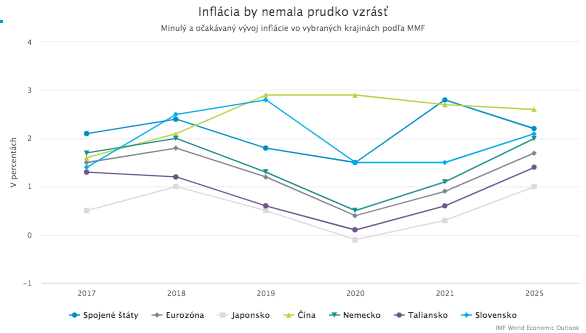

For advanced economies, the bigger problem will likely be low inflation

The current sharp rise in debt, together with a flood of liquidity from central banks, often raises fears of rapidly rising inflation. As we have emphasized in a previous article, however, higher inflation is not inevitable in the current situation.

On the one hand, there are indeed inflationary factors such as disruptions to supply chains, forced shutdowns of production in many firms, deglobalization impulses, and massive fiscal and monetary stimulus. On the other hand, the crisis also brought a massive demand shock caused by an overall decline in living standards, rising unemployment, and economic uncertainty leading to postponed spending and increased savings.

The IMF assumes these deflationary factors will keep inflationary pressures in check. Advanced economies therefore are unlikely to grapple with wildly rising inflation in the coming years; rather, similar to previous years, they will face insufficient inflation below the inflation targets of their central banks.

It will, however, be important for central banks to maintain credibility and, in the event of inflationary pressures, to prioritize price stability over keeping borrowing costs low for their governments. Otherwise, inflation could rise very quickly.

What to do to mitigate the crisis’ impact and restart growth?

As the text above makes clear, the global economy is in an exceptionally difficult situation today and the risks are enormous. Successfully managing the economic consequences of the pandemic will require not only great effort, but above all the right policies with appropriately set priorities.

The IMF recommends that governments, in the acute phase of the crisis, set the saving of lives and livelihoods as an absolute priority and devote as many resources as necessary to that end, regardless of budget deficits. Such a recommendation may be surprising coming from an institution that has traditionally been fiscally conservative.

According to the IMF, a temporary breach of fiscal discipline is justified and acceptable today, provided that after the crisis countries return to fiscal discipline. Inaction would cause much bigger problems and inflict even deeper wounds on the economy. The IMF also urges governments not to end support programs too early, before the virus is under control and the economy is well on its way to recovery. A premature withdrawal of state support could push the economy back into recession.

Once the acute phase of the crisis passes, governments should redirect resources toward public investment in areas such as infrastructure, education, science and research, healthcare, and the “green” economy. IMF research shows that properly targeted public investment not only raises the economy’s long-term potential, but in times of high economic uncertainty also has a large immediate impact on GDP growth and employment, as it attracts private investment. Increasing public investment by 1% of GDP could, under today’s conditions of high uncertainty, lead to as much as a 2.7% increase in global GDP, a 10% rise in private investment, and the creation of 20 to 33 million jobs.

At the same time, even after the crisis ends, it will be necessary to maintain support for those most affected. This is desirable not only from a social perspective; according to the IMF, it will also help the post-crisis recovery, since low-income people spend a high percentage of their income on consumption, thereby supporting overall demand in the economy.

Supporting the economy in the acute phase of the crisis and during the subsequent recovery will, of course, require substantial resources. The IMF recommends that countries cover the need for additional resources by issuing bonds with the longest possible maturities, thereby fully taking advantage of today’s record-low interest rates. They should also consider introducing progressive taxes, a wealth tax, and improving international coordination in collecting taxes from large multinational companies. Doing so would not only raise additional budget revenue, but would also reduce the previously mentioned acceleration of inequality.