U.S. Stocks Rise Despite Unrest, the Pandemic, and Record Unemployment

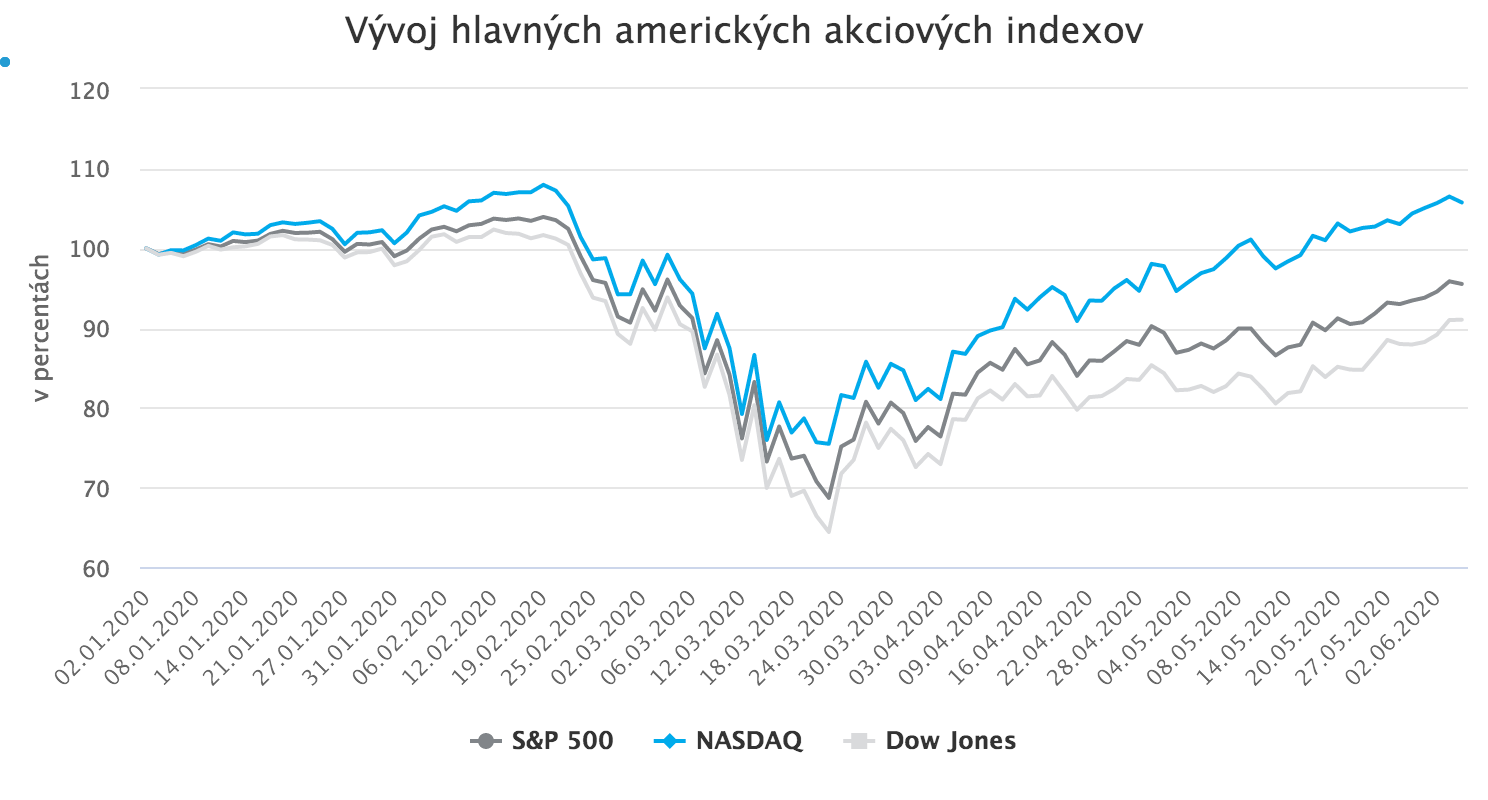

Major U.S. equity indices have been climbing almost uninterruptedly since the second half of March. Over that period, they have gained more than 40%, erasing almost all of the losses suffered during the initial pandemic-driven sell-off. The S&P 500 and the Dow Jones are now only a few percentage points below their previous highs. The Nasdaq has already reached new record levels, hitting fresh highs on Thursday.

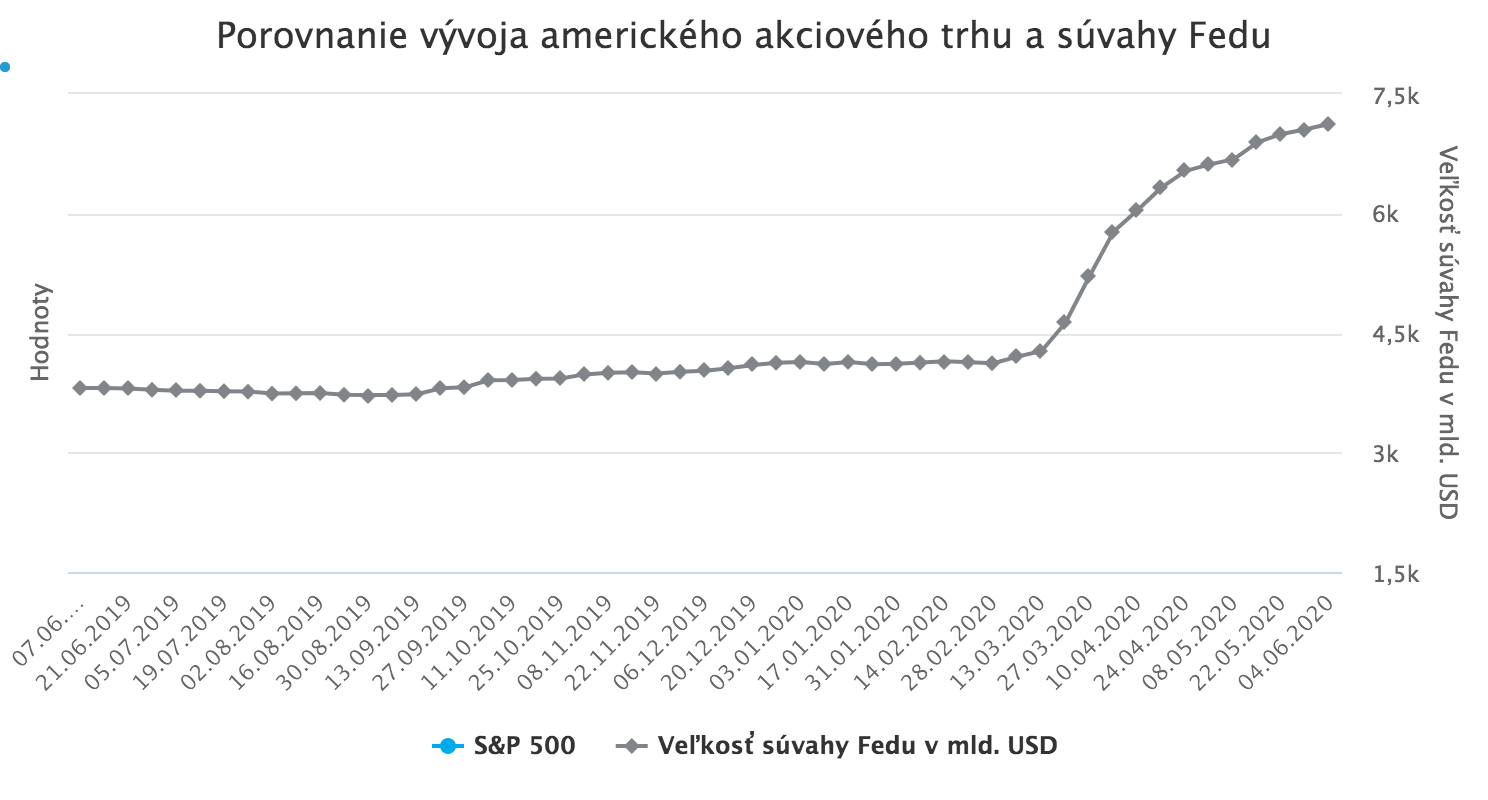

As we discussed in detail in a previous article, the fact that equities are rising in the midst of the worst economic collapse in modern history is not, in itself, as surprising as it may appear. The rally has rational drivers, although not necessarily the ones many would expect. In today’s environment, equity markets reflect less the performance of the real economy and more the availability of liquidity in the financial system. And because major central banks, led by the Federal Reserve, responded to the crisis with massive quantitative easing, effectively “printing money,” markets are currently awash with excess liquidity looking for a home.

If equities were consumer goods, today’s price increases driven by fresh money would be called inflation. Because they are investment assets, the same phenomenon is typically described as “gains” or “strength.”

The composition of the indices matters as well. Benchmarks are dominated by the largest, strongest companies in the economy, those best positioned to weather “hard times” thanks to cash buffers, superior access to financing, and, in some cases, direct or indirect government support. A growing share of U.S. indices is also made up of technology companies, a sector that has been among the least affected by the current crisis and in some respects has even benefited from it.

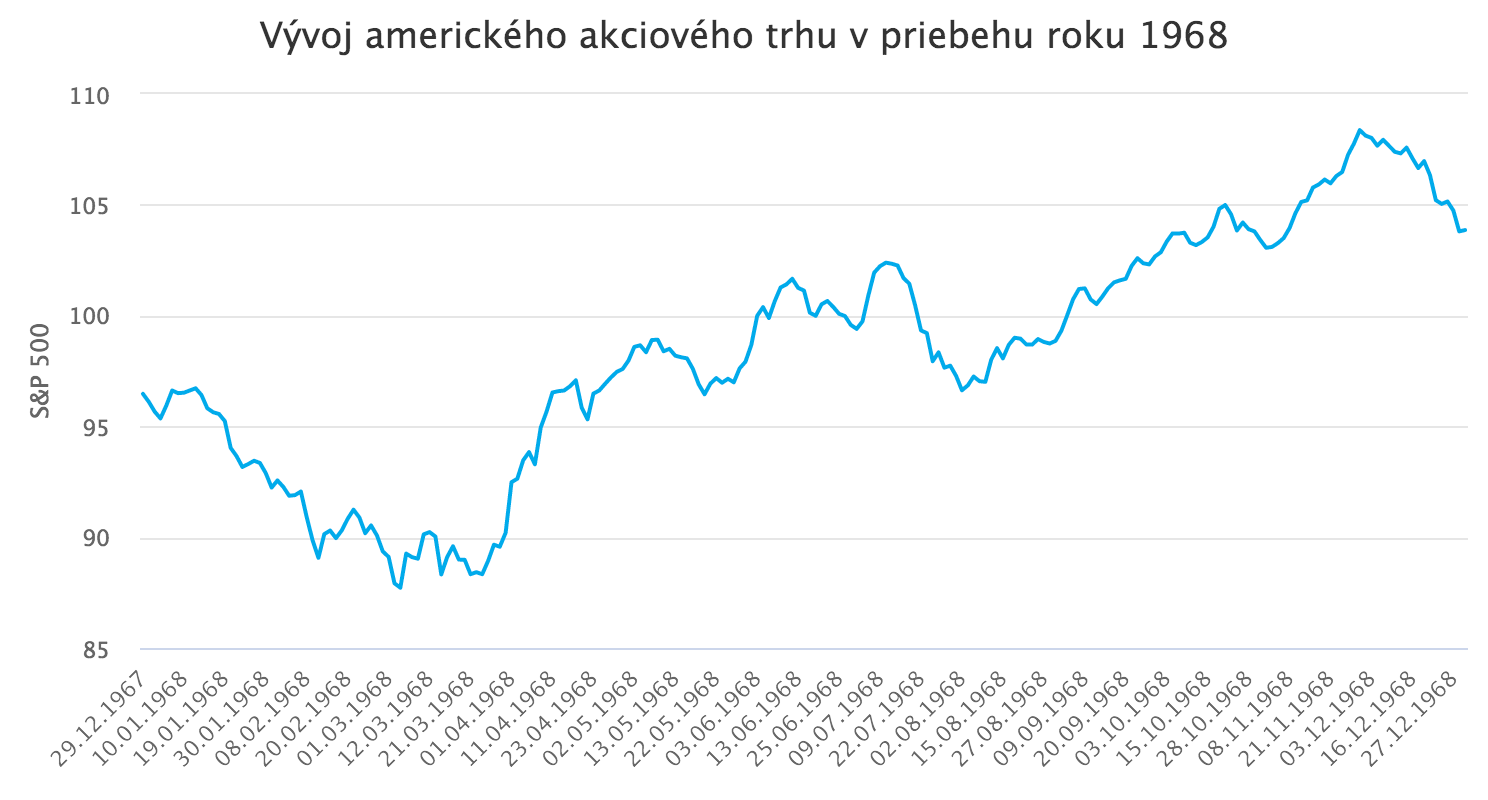

Meanwhile, equity markets typically react very little to protests and demonstrations, as their direct impact on the economy, and especially on the largest companies represented in the indices, tends to be limited. A one or two percentage point hit to GDP is not decisive in an environment where second-quarter output could, in the worst case, fall by as much as 50%. U.S. equities even rose in 1968, during one of the country’s most turbulent periods of civil unrest following the assassination of Martin Luther King Jr.

Still, the image of steadily rising equity prices against a backdrop of shattered shopfronts, looting and violence in the streets, a deep recession, an ongoing pandemic, and a historic spike in unemployment carries an undeniable air of absurdity, evoking comparisons to the “last days of Rome.” Among investors, the rally has earned the label “the most hated equity rally in history.” That alone is not sufficient to reverse it. But the current environment is nonetheless a volatile mix of risks that could still derail the rally, and for now investors appear to be underestimating them.

The unrest could not have come at a worse time

The current wave of unrest has arrived at the worst possible moment. Many U.S. states were in the process of reopening their economies after the forced lockdown triggered by the coronavirus. Protests and looting threaten those plans in at least two ways.

First, violence and curfews naturally deter people from returning to shops and restaurants, or, more precisely, from returning in a manner that would generate meaningful revenue for businesses. Second, mass demonstrations could easily contribute to a second wave of infections. Looting also inflicts additional damage on businesses already weakened by months of closures.

Chicago Mayor Lori Lightfoot captured the tragedy succinctly:

“It is heartbreaking that businesses that were preparing to reopen on June 3 after a long closure, building patios and getting ready, are now experiencing despair instead of a celebratory atmosphere.”

The longer businesses remain closed, and the greater the damage from looting, the closer they move to bankruptcy. For large listed companies, these losses may not be existential, but the demand shock will be felt. Moreover, the more businesses fail and the more people lose jobs and income, the longer and more intense unrest can become.

Compounding the problem, the U.S. Senate has postponed discussions on the next relief package, which had been scheduled for this week. That is unlikely to support a recovery or help stabilize the social climate.

Rising social tensions and the election calendar

Investors’ relative indifference to the unrest is partly rooted in the assumption that it will prove temporary and will not materially shape political outcomes. That expectation could turn out to be wrong.

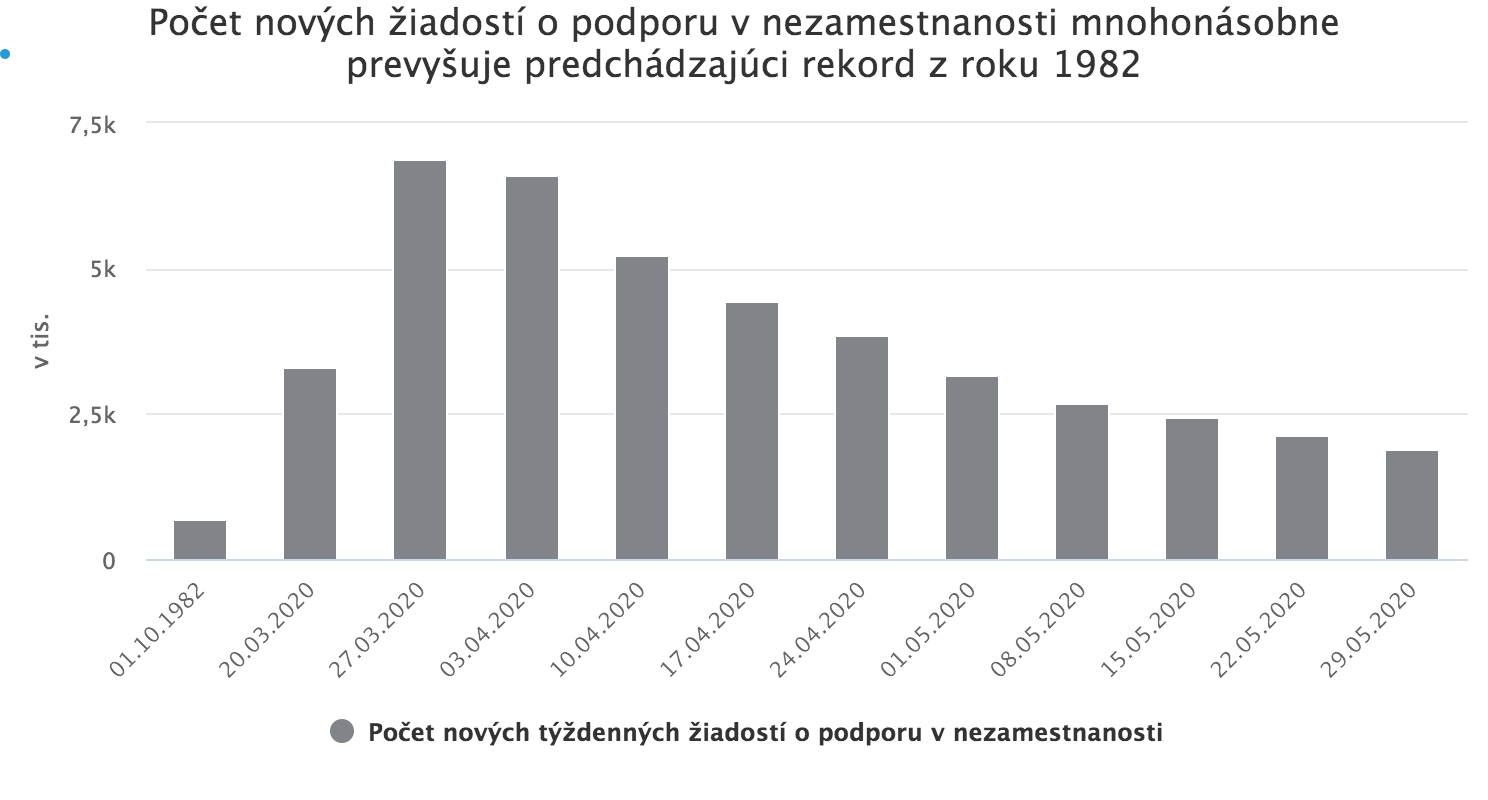

While the immediate trigger was the death of George Floyd, it is clear that this event was merely the catalyst. In a country where nearly 43 million people have filed for unemployment in less than three months, with losses concentrated among lower-income groups hit hardest by the crisis; where society is deeply polarized; and where wealth inequality is the highest in at least 50 years, almost anything can serve as a spark. Even if this wave of unrest subsides, further episodes appear likely.

Even if unemployment were to miraculously halve by the end of summer, it would still remain near levels seen at the peak of the previous crisis. Meanwhile, central bank “money printing” inflates asset prices, including equities, thereby exacerbating wealth inequality, as financial assets are disproportionately held by the wealthiest households. This environment creates near-ideal conditions for rising social tension.

The political backdrop adds another layer of uncertainty. U.S. presidential elections are scheduled for early November and the current environment will almost certainly shape the outcome. For now, it appears to improve the chances of a Democratic victory under Joe Biden. A Democratic win would likely entail rolling back Trump’s corporate tax reform, which reduced the effective tax rate for companies in the S&P 500 from 26% to 18%. A return toward previous tax levels would mechanically lower expected earnings (Goldman Sachs estimates by an average of about 11% over the next year), a shift that would have a material negative impact on equity valuations.

Uncertainty in the White House

Another, and perhaps the largest, risk factor is the current occupant of the White House. Trump’s conduct during the crisis has been even more volatile and controversial than before, creating significant uncertainty and a wide range of open questions, many of which matter for the economy and markets.

Will he attempt to divert attention from domestic problems by escalating international conflicts, particularly with China, including through renewed trade war measures? Or will he focus on domestic issues and leave China, Russia, Turkey, Iran, and Saudi Arabia greater freedom in shaping regional and global disputes? Will his response to the protests inflame tensions further or help defuse them?

If he feels politically weakened, will he intensify attacks on social media platforms and technology companies, which today carry the greatest weight in equity indices? Will he seek to break up Amazon (as he has previously threatened) in response to critical coverage in the Washington Post, owned by Jeff Bezos? Or might Democrats pursue antitrust action against these monopolies if they win?

And if Trump loses, will he accept the result, or could the country face yet another wave of civil unrest?