Why are our pensions low?

How does employment affect pensions?

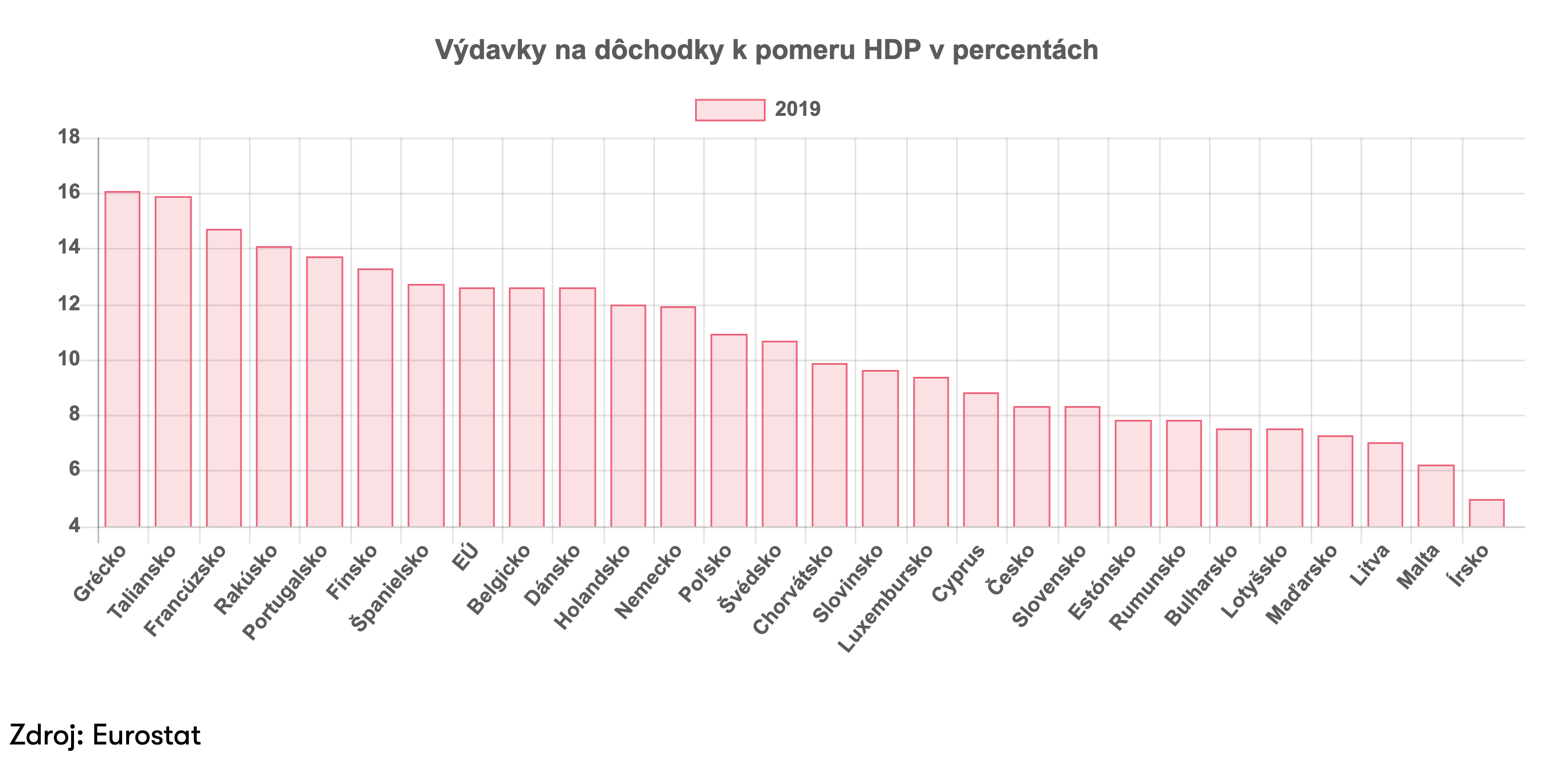

State pensions in Slovakia, as in most EU countries, are paid from contributions made by currently employed workers. The more people who work and pay contributions into the system, the better the state can provide for current pensioners. Equally important is the ratio of workers to pensioners. Many working people remain under a mistaken impression: they believe the state holds their paid contributions in an individual account and will pay them back in old age. This is an incorrect assumption and could have dire consequences in the future, given unfavourable demographic trends in our country. Pensions will therefore probably be lower in the future than they are today, and relying solely on the state may be very risky.

How can I influence the level of my pension?

Slovakia is not a pioneer in pension systems, but fortunately we can sometimes adopt good practices from abroad. One such solution is the multipillar pension system. These pillars help secure a better pension — but how many pillars does Slovakia’s system have and what are the differences? The Slovak pension system is built on three pillars. The first pillar is compulsory pension insurance; the second pillar is oldage pension saving; and the third pillar consists of supplementary pension savings.

As the names indicate, the first pillar is mandatory insurance and every employee or selfemployed person is covered under this scheme. The first pillar is nonheritable and is administered by the Social Insurance Agency (Sociálna poisťovňa). Entry into the second pillar is voluntary. If an individual opts in, the contribution paid to the Social Insurance Agency is split: part goes to a pension management company and part remains in the first pillar. Entry to the second pillar is only possible up to the age of 35, regardless of whether the person is currently employed.

The advantage of the second pillar lies in its inheritability and in the ability of contributors to choose how their contributions are invested; voluntary topups are also permitted. Finally, the third pillar serves as a supplementary element of the overall pension scheme. It is an additional way to improve one’s pension, but this form of saving only makes sense if the employer is prepared to contribute on the employee’s behalf. The thirdpillar pension is also inheritable and the invested funds are managed by a supplementary pension management company. Savers also benefit from a tax allowance: contributions up to EUR 180 may be deducted from the tax base.

A policyholder may therefore choose from the options described above and thereby influence their future pension. For illustration, index funds have historically offered an average annual return of around 9% since inception; equity funds about 3%; mixed funds 2.5%; and guaranteed bond funds 1.3%. According to ViceGovernor Ľudovít Ódor, with a betterdesigned second pillar we could have had approximately EUR 10 billion more on pension accounts than we do today, whereas the current volume stands at roughly EUR 12 billion. Of course, past returns do not guarantee future performance, but historically the longer the saving horizon, the more riskoriented an investment instrument a saver can reasonably choose.

Working in the EU — will I be entitled to a pension?

An EU citizen need not fear that years worked in other Member States will be disregarded. All years worked will be taken into account, and entitlement will depend on the country or countries in which the claimant becomes eligible for a pension. The process will be handled by the Social Insurance Agency or by the competent authority in the country where the claim is lodged. The EU’s coordination of social security also covers certain other states — specifically Norway, Iceland, Liechtenstein and Switzerland — so periods worked in those countries will likewise be recognised. This ensures social fairness across the European area.

Read the previous article in the pension series: Part 1.

Disclaimer

All texts, images, graphics and other objects contained in this document are protected by copyright. Without the prior written consent of Sympatia Financie, o.c.p., a.s., the content of this document may not be copied, distributed, altered or provided to third parties. This document contains general information only. Sympatia Financie, o.c.p., a.s. does not provide any professional advice or services through this document and accepts no liability for any loss arising directly or indirectly from reliance on its contents.