Will the equity market continue to fall?

Price collapses of more than 80% on stock exchanges are not unusual. The Nasdaq index is now firmly in a bear market. Among the most popular stocks that have been heavily hit are Spotify (70%), Teladoc (70%), Palantir (80%), PayPal (75%), Netflix (75%) and Facebook/Meta (55%). Market volatility is exactly what speculative investors are exploiting today, and their activity is significantly aggravating the situation.

Bulls’ vs bears

A bull is an investor who is optimistic and expects stock prices to rise; a bear is pessimistic and forecasts a market decline. These two camps ultimately determine market direction. Over the long term, bulls have generally prevailed, since most equity indices rise over extended periods. Today, however, the financial market is undergoing a correction and shortselling, pessimistic investors are reaping large profits.

Why did the bull run end?

There is no simple answer — many factors interrupted the long upward trend. The most important include overvalued equities, high inflation, the war in Ukraine, rising bond yields and a change in monetary policy. Regarding overvaluation: for example, Nasdaq’s pricetoearnings ratio (P/E) fell from 36.9 to 19, which is roughly the valuation level seen during the Covid19 market low. Of course, this does not mean the market correction is over and that one should buy blindly. Each investor must evaluate the current situation and all the fundamental risks of investing. Equities are therefore not necessarily the right choice for everyone. An alternative to stocks is real estate, which even in today’s uncertain environment can offer a defensive investment with solid returns — a segment that many property investors favour. Another factor weighing on sentiment is high price levels, which typically dampen market mood. Investor concerns are particularly pronounced for highly indebted and lossmaking companies, since it is uncertain whether they can survive in an environment of expensive financing and margin pressure. In periods of high inflation, companies that can effectively pass on higher costs into their margins tend to fare best; those that succeed will emerge from the inflationary shock as winners.

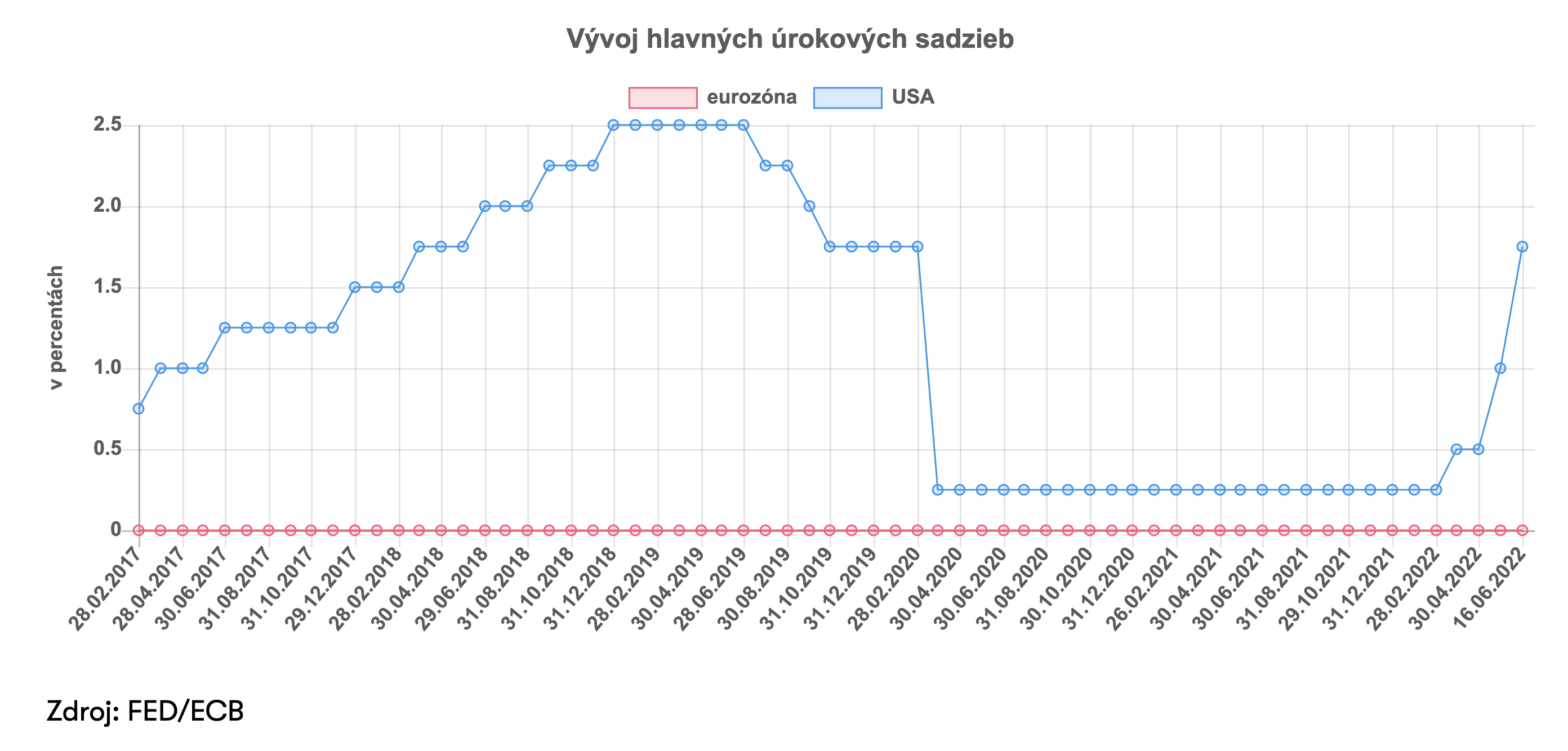

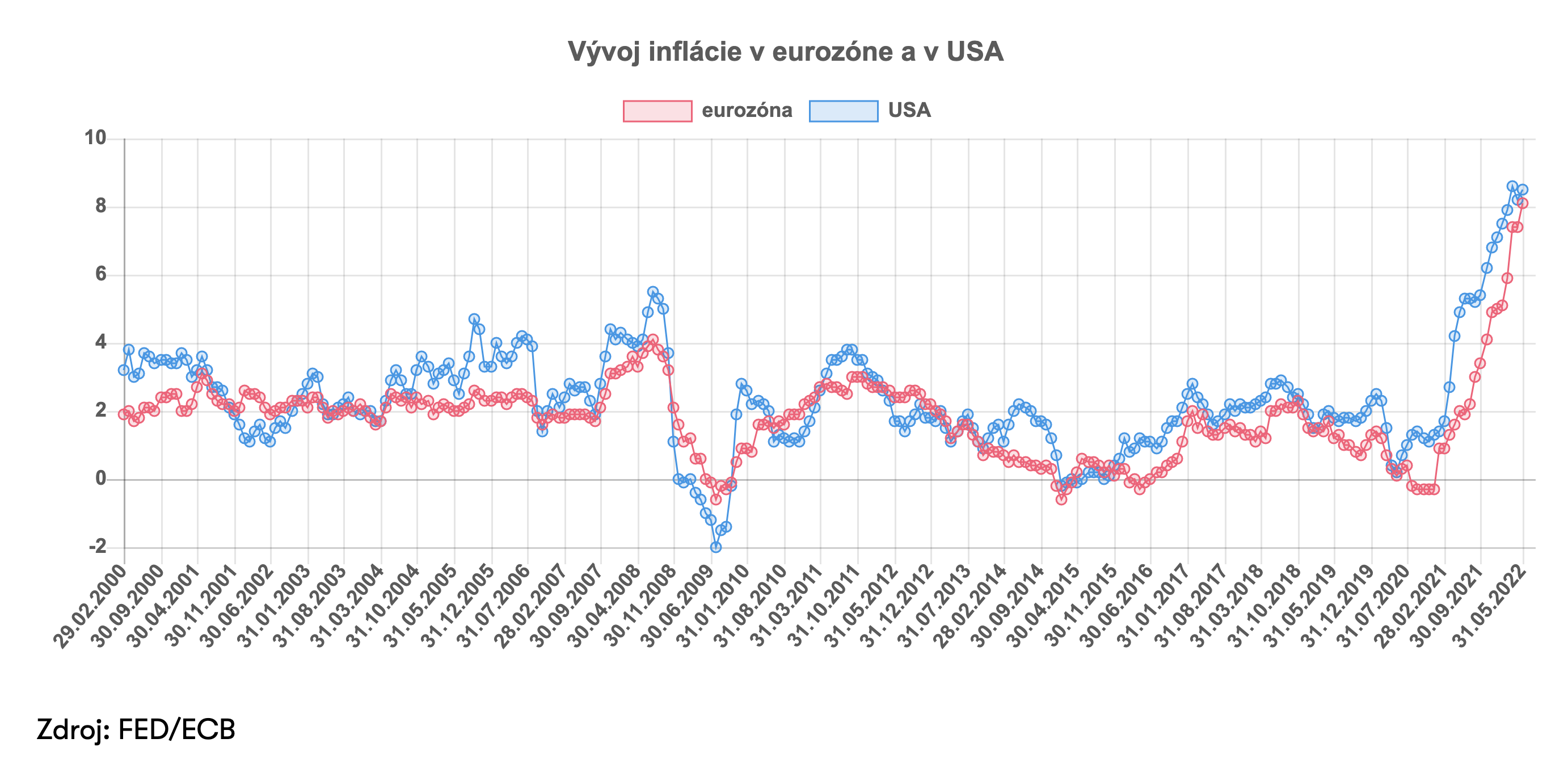

How are the Fed and ECB responding to rising inflation?

Inflation hit the United States earlier than the eurozone, so the central banks are at different stages in their responses. The Federal Reserve has already begun raising its policy rate and intends to continue until inflationary pressures ease. The current policy rate stands at 1.75% and the Fed chair has signalled plans to raise the key rate by at least 0.5 percentage points at upcoming meetings. In addition, the Fed has begun reducing its inflated balance sheet of nearly USD 9 trillion. The European Central Bank has so far kept rates at zero or in negative territory. The ECB faces a different situation because core inflation has not reached the same levels as in the US. Nevertheless, signals are emerging that monetary policy will normalise: rate increases in euro area countries are anticipated already in the summer. The ECB president remains cautious — unsurprisingly, since aggressive rate hikes could place several highly indebted eurozone countries (for example Italy or Greece) in a precarious position.

Recession is knocking on the door

It is no secret that the economy moves in cycles of rapid expansion followed by cooling. A technical recession is approaching in the US and is likely to hit the eurozone as well. The United States has already recorded one quarter of negative GDP growth (1.4%); a second negative quarter would officially constitute a recession. Slowing growth is being driven by rising interest rates, high inflation and deteriorating business and consumer sentiment. Everyone is more cautious in their spending, which strongly affects money flows through the economy. Growth forecasts are being revised downward by major institutions. The UN has cut its global GDP growth outlook from 4% to 3.1% and expects inflation to rise to 6.7%, roughly double the decade’s average. The European Commission has likewise downgraded its growth projection for this year, lowering expected GDP growth in the EU from 4% to 2.7% while forecasting inflation of 6.1% compared with its previous 3.5% projection. Few now doubt that inflation will materially impoverish people and that some regions may experience a short recession. Once inflation is brought under control and the war in Ukraine ends, economic sentiment could improve.

Disclaimer

All texts, images, graphics and other objects placed in this document are protected by copyright and, without the prior written consent of Sympatia Financie, o.c.p., a.s., the content of this document may not be copied, distributed, modified or provided to third parties. This document contains only general information. Sympatia Financie, o.c.p., a.s. does not provide any professional advice or services by means of this document and accepts no liability for any damage arising directly or indirectly in connection with any person who relies on this document.