The fire in the Black Garden burned the lira and the ruble.

Nagorno-Karabakh, also known as the Black Garden, has a complex and bloody history. Armenia and Azerbaijan have disputed this territory for decades. The most intense fighting broke out after the collapse of the Soviet Union and claimed thousands of lives. The 1994 peace agreement officially ended the war, but the dispute itself was not resolved. Like several other conflicts in the region, it merely froze indefinitely after the peace deal, while smaller clashes and border skirmishes continued.

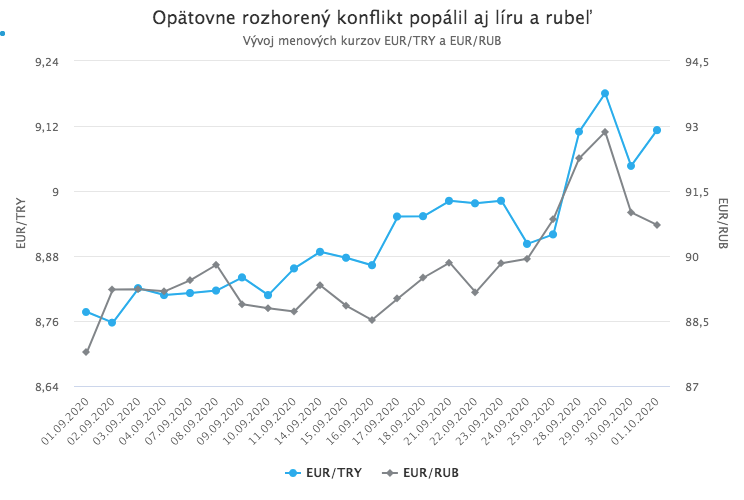

However, the fighting that erupted on 27 September represents the most serious escalation to date, one that could plunge the entire area back into a full-scale, open war. Given the region’s complex political situation and its proximity to critical oil infrastructure, such a development would not only cause an enormous human tragedy, but would also bring serious economic consequences extending beyond the borders of Armenia and Azerbaijan. Early signs of this were already visible in the markets on Monday, 28 September, the first trading day after the outbreak of the conflict. It was not only Armenian and Azerbaijani assets that declined; the Turkish lira and the Russian ruble also weakened sharply.

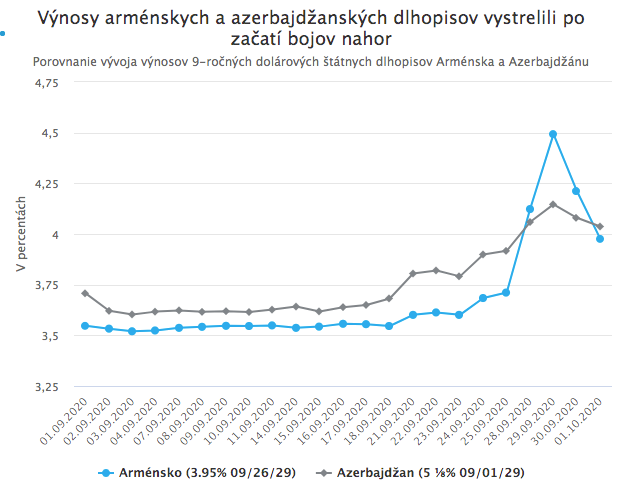

The outbreak of fighting is also visible in the bond market

The outbreak of hostilities naturally had the most direct impact on the bonds of Armenia and Azerbaijan, the primary parties to the conflict. As can be seen in the chart below, government bond yields in both countries jumped immediately after the fighting began, with the initial rise in yields being sharper for Armenia than for Azerbaijan.

We would like to remind you that there is an inverse relationship between bond yields and their prices; a rise in government bond yields is therefore the result of a decline in their prices. Higher yields thus reflect higher risk, and if the increase is more persistent, they raise governments’ interest costs and make it more difficult to raise funding in the markets.

The relatively sharper rise in yields on Armenian government bonds in the first days of the conflict likely reflects the fact that, according to qualified estimates, Azerbaijan currently has a stronger and better-equipped military than Armenia, and that its ally Turkey immediately came out in its support. Investors therefore attributed greater risk to Armenia. However, as the chart shows, the situation stabilized slightly in the second half of the week and Armenian bond yields again moved a few basis points below Azerbaijani yields, where they have been over the long term. Nevertheless, yields in both countries remain elevated and are likely to remain volatile in the coming days.

4% for the risk of all-out war

If we were to trust the signals from bond markets, the situation is not serious so far and an all-out war does not appear imminent. The rise in yields to slightly above the 4% level was sharp, but yields around 4% are not dramatically high. Countries on the verge of economic collapse typically have yields several times higher. The problem, however, is that bond-market signals in this case are not reliable indicators of the true risk. The flood of liquidity provided by central banks after the outbreak of the coronavirus crisis has distorted bond markets and “artificially” pushed yields lower worldwide, weakening their signaling function.

Moreover, as has been shown repeatedly, markets often do a poor job of estimating and pricing extreme risks (tail risks), especially in the case of countries that are typically on the periphery of investors’ interest. Lending for nine years at 4% per year to a country that is in a military conflict with a neighboring state, where the conflict could at any time escalate into all-out war, and in a region that is like a tinderbox, simply does not look like a sensible investment with a good risk-return trade-off.

In any case, the total outstanding volumes of Armenian and Azerbaijani bonds are very small from the perspective of the global bond market. Any dramatic moves in them (if the conflict were to slide into all-out war) would therefore have a significant impact only on the portfolios of their holders and should not spill over into other markets. That cannot be said, however, of the lira, the ruble, and oil, which are also affected by this conflict.

The fire of fighting also burned the lira and the ruble

The risk of the entire conflict and its possible consequences (not only economic) is dramatically increased by the fact that it is not limited to Armenia and Azerbaijan, but also involves Turkey and Russia closely. These are countries that are already fighting each other through proxy wars in Libya and Syria.

Turkey openly and loudly supports Azerbaijan and declares that it should retake, by military means, territories that it claims rightfully belong to it. Turkey is also supplying the country with military equipment and appears to be providing jihadist fighters from Syria as well. Russia is historically an ally of Armenia, and the two countries are bound by a mutual defense alliance, the Collective Security Treaty Organization. In the current situation, however, Russia is not as unequivocal an ally of Armenia as Turkey is of Azerbaijan. It is simultaneously trying to maintain good relations with Azerbaijan, and the defense treaty that would theoretically oblige it to help Armenia does not apply to Nagorno-Karabakh, since it lies within Azerbaijan’s territory and is not considered part of Armenia.

A potential all-out war between Azerbaijan and Armenia that would not be limited only to the territory of Nagorno-Karabakh would likely obligate Russia to assist Armenia. There is therefore a risk that, in the event of an escalation, Turkey and Russia could ultimately find themselves facing each other on the battlefield. This significantly increases the overall risk of the conflict. A less extreme scenario, in which the two countries would not fight openly against each other but the conflict would turn into a prolonged proxy war similar to those in Syria or Libya, is also highly unfavorable, as this region has a strategically crucial position between Russia, Turkey, and Iran, and it is crossed by important energy infrastructure.

These concerns were reflected in the markets immediately after the conflict broke out. The Russian ruble and the Turkish lira both weakened sharply on Monday (28 September) after markets opened. The Turkish lira fell to a new low. Against the euro, it crossed the 9 EUR/TRY threshold for the first time. The ruble, in turn, moved further beyond 90 EUR/RUB and, if we exclude a brief spike shortly after the annexation of Crimea, it is also at historical lows.

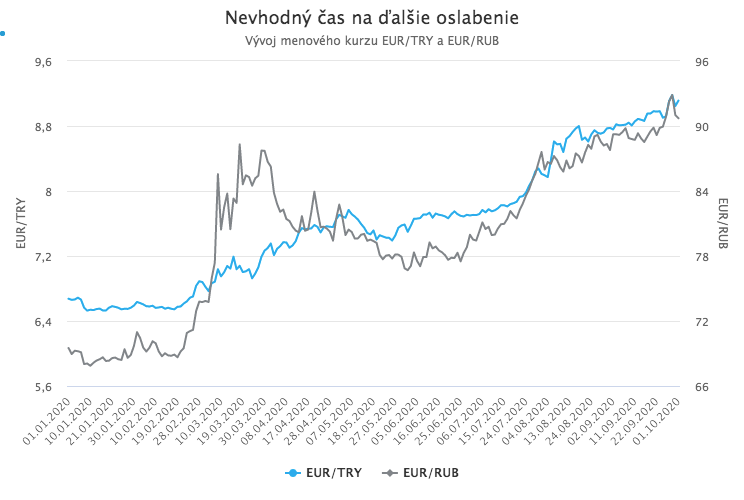

Unfavorable timing

For both currencies, this conflict flared up at a very unfavorable time. The lira and the ruble are the first and second weakest currencies among emerging markets this year. Both have lost more than 20% since the beginning of the year, and their weakening has accelerated in recent weeks. In the case of the ruble, this was mainly due to concerns about possible sanctions related to the poisoning of Alexei Navalny. In the case of the lira, it was due to persistently high inflation in the country, combined with Erdoğan’s reluctance to allow the central bank to raise rates, the risk of a balance-of-payments crisis, and, at the same time, Turkey’s aggressive actions in the Eastern Mediterranean, which also “smell” of sanctions.

It is worth noting that although Erdoğan had long refused to allow interest rate hikes, even though they would have helped the lira, last Thursday he gave the central bank the green light, and it surprisingly raised the key policy rate by as much as 2%. This move was unexpected, and the lira reacted by strengthening significantly. Had it not been for this rate hike two trading days before the conflict began, the lira would have weakened even more this week.

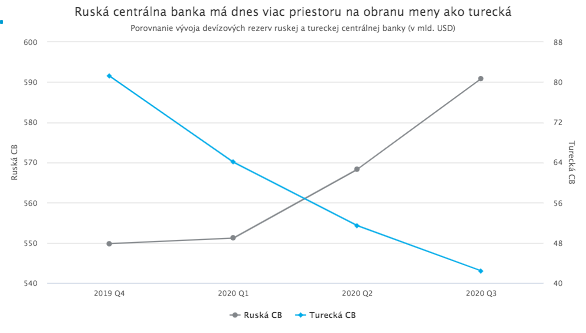

It is therefore an interesting question whether Erdoğan was prompted to accept the first rate increase in two years precisely by the expected outbreak of the conflict and its impact on the lira. In any case, if the conflict continues to escalate, both currencies will face strong pressure to weaken further. The ruble, however, is in a better position to withstand this pressure with less damage than the lira, since the Russian central bank today has significantly more room to support the ruble than the Turkish central bank. This is also evident from the trajectory of foreign exchange reserves at the two central banks.

At the same time, the weakening of the lira is a relatively more serious problem for Turkey, which faces greater challenges in servicing its high external debt. Continued depreciation of the lira could therefore create difficulties in repaying foreign-currency liabilities and could even lead to default. Such a development would already cause problems for European banks as well. The largest exposure to Turkey, worth as much as USD 46 billion, is held by Spain’s BBVA.

Oil infrastructure at risk

Another risk of the current conflict lies in its potential impact on energy infrastructure. The region is an important hub for transporting both crude oil and natural gas from Central Asian producers to Turkey and onward to European markets (especially Greece and Italy) as well as Asian markets. Of particularly high strategic importance are the BTC oil pipeline (Baku-Tbilisi-Ceyhan) and the South Caucasus gas pipeline (Baku-Tbilisi-Erzurum).

So far, this risk has not visibly materialized in the oil market, as oil prices are currently falling due to the second wave of the coronavirus and concerns about its impact on a renewed decline in oil demand. This factor will likely continue to weigh heavily on oil prices in the coming weeks and keep any upward pressure in check. Therefore, unless the current conflict slides directly into the deliberate destruction of oil infrastructure, it is unlikely to lead to a more significant rise in oil prices.

In previous escalations, Armenia and Azerbaijan have generally avoided damaging energy infrastructure, although Gazprom announced in July this year that its Armenian gas pipeline had been damaged. It did not specify the cause, but the timing and location corresponded to shelling by Azerbaijan during one of the smaller escalations. In the event of an all-out war between Armenia and Azerbaijan, with the involvement of Turkey and Russia, however, no scenario can be ruled out, including the destruction of energy infrastructure in the region.