Bad Data Are (Sometimes) Good Data

What is bad for the real economy is not always bad for equity markets. Sometimes it is even exactly the opposite. That was the case this week as well. US equity markets responded to weak data from the US economy by rising to new highs. At first glance, such a development may seem nonsensical; however, investors today assess all US economic data through the lens of their implications for the Fed’s next steps. Weak data mean that the Fed will not rush to end its extremely accommodative monetary policy, on which markets are now literally dependent.

Slower GDP growth

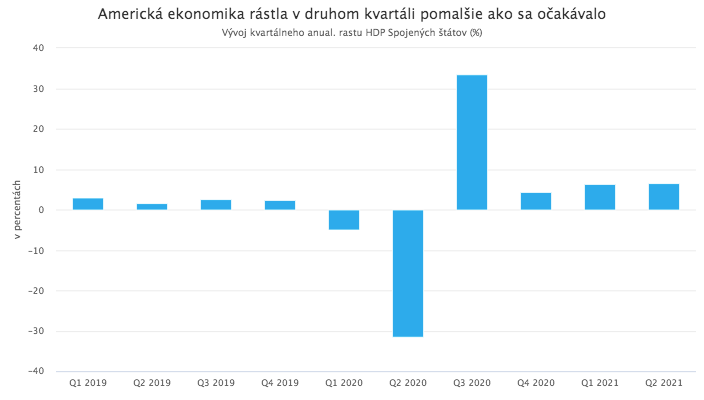

Data released this week showed that the US economy grew more slowly in the second quarter than expected. The consensus estimate among economists was for 8.4% GDP growth, but the actual figure ultimately came in at only 6.5%.

Of course, such a growth rate cannot in itself be described as weak, especially if we take into account that US GDP grew at a similar pace in the first quarter, while most European economies were still struggling with a strong second wave of coronavirus and instead of growing were stagnating or even contracting. Thanks to this, the US economy has already returned to pre-pandemic levels. According to the European Commission’s latest forecast, euro area economies will reach this milestone only at the end of the year. It is also positive that personal consumption, which plays a key role in the US economy, rose by as much as 11.8% in the second quarter, more than economists had forecast, despite the overall GDP figure falling short of expectations. Despite these positives, however, it is simply a fact that the US economy grew more slowly in recent months than expected. Its aggregate growth rate for the first half of the year reached 6.4%. This means that if it were to grow this year in line with the Fed’s forecast, it would have to grow at a rate of at least 7.4% in the second half. That is a difficult target to achieve in the coming months, also given concerns about the Delta variant and the impending expiration of several support schemes for households and the economy. It therefore seems likely that the US economy will deliver a weaker performance this year than the Fed assumed, and this fact will undoubtedly influence its future decisions.

Weak labor market data

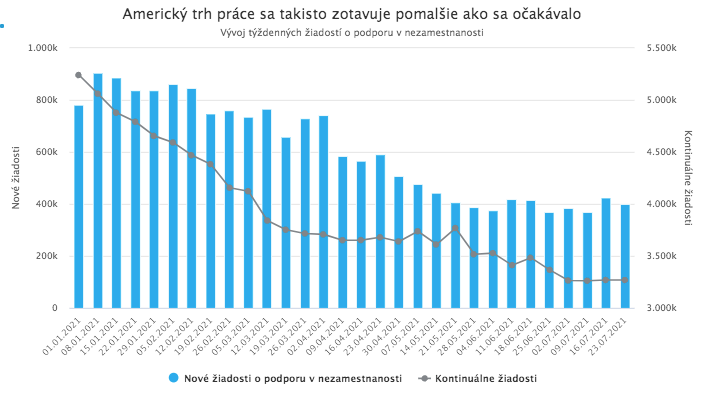

Fresh figures from the US labor market, released on the same day as the GDP data, were also disappointing. They showed that the labor market is likewise not recovering at the pace that had been expected. The number of new weekly unemployment benefit claims reached 400 thousand. The consensus estimate among economists was 20 thousand lower. The figures for the previous week were moreover revised upward, to the highest value since May, and continuing claims also came in higher than expected.

These data are thus further evidence of persistent imbalances in the US labor market. Unemployment is not declining at the expected pace, and that is also a factor that will significantly affect the Fed’s decision-making regarding its next steps. Unlike most other central banks, the Fed has a dual mandate, which commits it to pursue not only price stability but also “maximum employment.” For decades, the employment objective was defined as “full employment.” It was adjusted to the current concept of “maximum employment” only in the summer of last year in light of the devastating social impacts of the pandemic. This is not a cosmetic change. In this case, the change of a single adjective has significant meaning. “Full employment” is now to a large extent an outdated economic concept, which gave the Fed a reason to tighten monetary policy, and thus dampen economic growth, as soon as falling unemployment put more pronounced upward pressure on wage growth. By changing the goal from “full employment” to “maximum employment,” the Fed wanted to emphasize that it would not only strive to achieve low unemployment, but also greater inclusiveness in the labor market and healthy wage growth. Its revised definition of the inflation target simultaneously allows it to pursue the goal of maximum employment even at the cost of a temporary increase in inflation. Labor market data therefore simply have a major impact on Fed policy today.

Markets’ dependence on the Fed

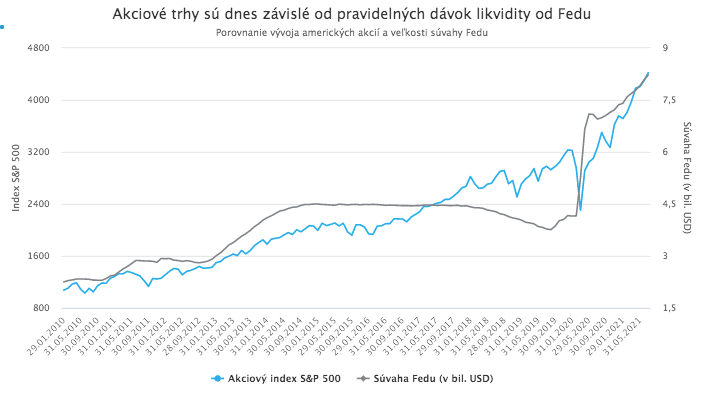

Investors’ tendency to analyze macroeconomic data primarily through the prism of their impact on Fed decisions is nothing new. It expanded especially after the global financial crisis, when the Fed sharply reduced interest rates and began quantitative easing, also referred to as “printing money.” Markets quickly became accustomed to regular doses of liquidity from the Fed, and whenever concerns arose that the Fed might reduce them, panic spread in the market. Today, liquidity has a greater influence on equity market moves than any other factor, including developments in the real economy.

This dynamic worsened after the outbreak of the pandemic. The Fed’s renewed cut of interest rates to zero and, above all, record levels of liquidity injections through quantitative easing bear the lion’s share of the credit for the equity market’s record-fast recovery from the initial pandemic sell-off and its continued strong growth to this day. At the same time, however, this has only deepened the market’s dependence on Fed support, as the Fed still “pumps” USD 120 billion per month into the markets and keeps interest rates at record-low levels. The idea that the Fed could limit this support is therefore a nightmare for markets today, but one that has been becoming increasingly realistic in recent months.

Bad data are good news for stocks

The US economy has already largely recovered from the crisis, markets have forgotten the pandemic sell-off, and consumer prices in the US are moreover rising sharply. These are factors that today give the Fed a good reason to proceed with a tightening of monetary policy, of course only very gradual and modest. Fed officials are aware of markets’ huge dependence on extremely accommodative policy, and therefore act extraordinarily cautiously and slowly not only in adjusting policy itself but also in signaling the changes they are preparing. Before raising rates, they must first reduce the volume of monthly bond purchases under quantitative easing; and before reducing purchases, they must announce this step sufficiently in advance; and before announcing it, they must signal to markets sufficiently in advance that they are beginning to consider such an announcement, so as not to trigger panic. In any case, the Fed has already completed the first step of this comically cautious and protracted process since last month. Investors’ current expectation is that a formal announcement of the tapering of purchases will come toward the end of this year, with a start date set for the first months of next year. The first increase in the main policy rate, by a quarter of a percentage point, will not occur earlier than in two years. After this week’s Fed meeting, Fed Chair J. Powell, despite his usual effort not to say anything material, more or less confirmed these expectations. And that is an unsettling prospect for markets.

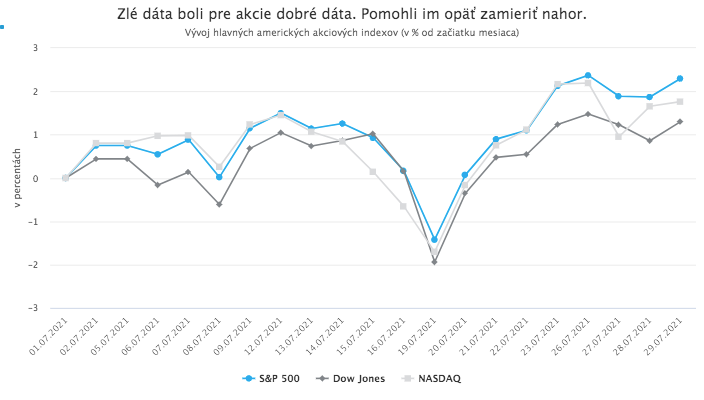

The series of weak macroeconomic data that arrived just one day after the July Fed meeting is therefore good news for markets. If the US economy grows more slowly this year than expected and the labor market does not move closer to the goal of “maximum employment,” the Fed may still reconsider reducing purchases from the current USD 120 billion per month, or at least postpone this “drastic” step by a few months. That was sufficient reason for US equity indices on Thursday to head again toward new highs. What excellent quarterly results from a handful of the largest technology companies could not achieve, weak macroeconomic data did.