First Quarter 2022

War in Ukraine

The reaction of the West and its allies came immediately after Russia’s military attack on Ukraine. Numerous economic sanctions were imposed, aiming to put pressure on the Russian Federation so that it would be motivated to end this unnecessary conflict as soon as possible. The sanctions were unprecedented in this case and targeted the central bank (freezing Russia’s foreign-exchange reserves abroad), the state, oligarchs, and they also aimed to reduce the population’s standard of living. Countless foreign companies left their business activities in Russia, even though they did not have to. Many important and luxury products are no longer exported to Russia. All of this has and will result in a significant weakening of Russia’s economy and a deterioration of living standards. Some estimates for 2022 speak of 20% inflation and an economic decline of up to 30%.

Stock markets

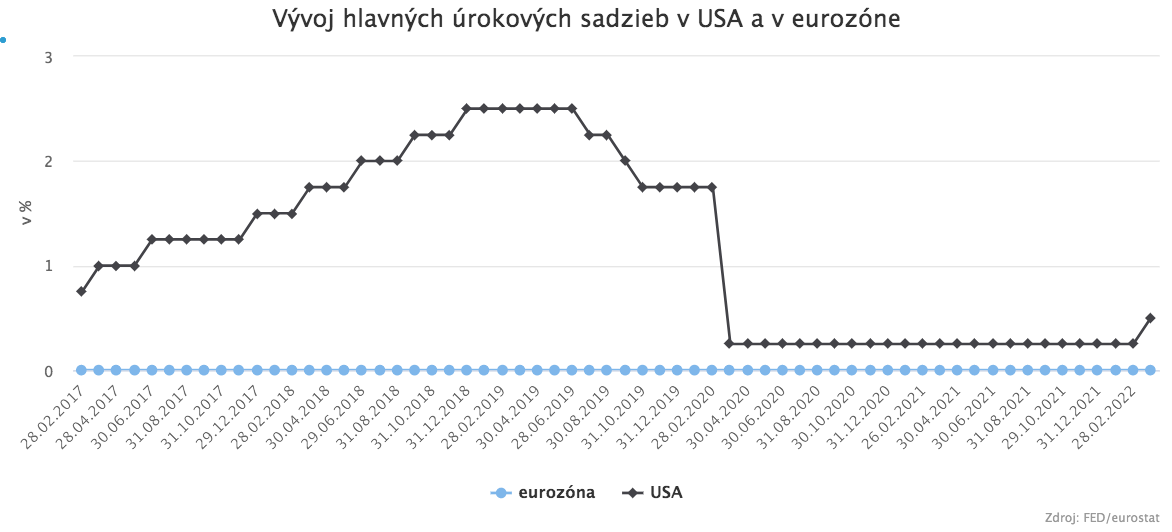

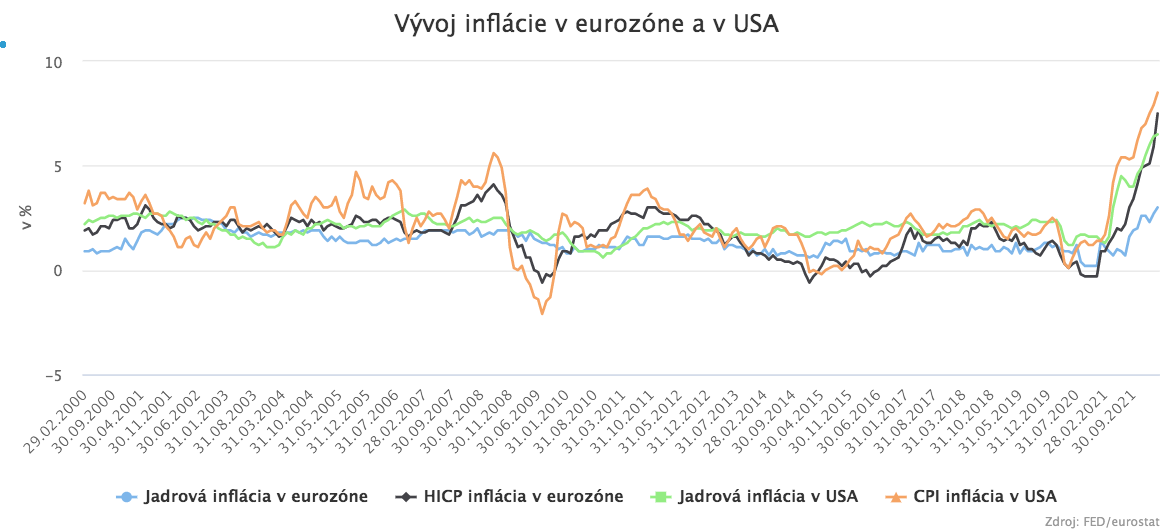

Financial markets failed to follow up on last year and ended the first quarter in the red. Specifically: the S&P 500, the best-known stock index (-5.55%); the Nasdaq, a mainly technology index (-10.18%); the Dow Jones Industrial (-5.21%); the EURO STOXX 50 (-9.91%); the Nikkei 225, the Japanese index (-5.05%); and the Hang Seng Index, the Chinese index (-5.49%). It is therefore clear that stock markets are under considerable pressure, even though most indices managed to erase the losses since the outbreak of the war. On the other hand, after such strong growth as we saw last year, a decline is a healthy reaction. Not to mention the correction in growth stocks, which in many cases lost more than 50% of their value. The market is therefore normalizing, also under the pressure of current events. The most frequently cited contributor to uncertainty is inflation. It is pushing central banks to raise interest rates. This will make corporate financing more expensive, and therefore this reality is reflected in stock market valuations. In addition, more expensive financing will slow economic growth, which again worsens the short-term outlook for equities. Rising inflation also raises the issue of corporate profitability. Companies try to pass higher costs on to consumers to some extent, but this is not always possible in full. The biggest contributor to higher inflation is largely energy. The energy component of the inflation basket contributes the most to price growth. Logically, these higher costs then spill over into other inflation components, although in the euro area this pass-through is slower than in the U.S. This is best seen by comparing headline inflation and core inflation, which excludes food, energy, alcohol, and tobacco. It is very important to watch the difference between these two macroeconomic indicators. In the U.S., inflation reached 8.5% in March and core inflation 6.5%, which is not such a large gap. In the euro area, inflation rose to 7.5% in March, while core inflation ended at 3%. This is precisely why the ECB is pursuing a much looser monetary policy than the Fed. Through their monetary tools, central bankers primarily influence core inflation, which in the euro area is not as alarming. Therefore, the ECB’s interest-rate increases will be slower, because high rates hardly affect energy prices, which have the greatest impact on price growth.

Bond market

The situation in government bonds changed significantly in the first quarter, and yields rose to levels investors had not seen for a long time. Interestingly, the U.S. yield curve moved into an inverted position, and yields on two-year, five-year, ten-year, and thirty-year bonds are practically the same. This suggests that in the short term, investors are concerned about holding government bonds because they expect economic problems. Yield-curve inversion usually predicts a recession; however, it does not have to, and it may simply reflect great uncertainty about how the conflict in Ukraine will end and where inflation will stabilize. German government bonds, representing the strongest economy in the euro area, returned to positive yields again after many years, which also suggests increased concerns about near-term economic developments. Not to mention that negative bond yields do not signal healthy development; on the contrary, they point to problems in monetary policy. Germany’s yield curve is currently also moving toward an inverted position, and this important indicator should continue to be monitored. The emergence of low to negative yields on German government bonds was caused by the ECB’s extremely loose monetary policy, under which it massively purchased bonds in the capital market.

Currency market

The forex market was truly turbulent this quarter. After the start of the war in Ukraine, the Russian ruble fell to historic lows and for a while traded with a loss of more than 40%. This was logically caused by panic in the market, as confidence in the Russian currency collapsed dramatically and acceptance of the currency was significantly limited. People therefore wanted to get rid of rubles and replace them with a stable currency, such as the U.S. dollar or the euro. Later, the Russian government led by Putin managed to artificially stabilize the domestic currency, but only thanks to strict restrictions. First, the Russian central bank raised the key interest rate to 20% (currently 17%), which supports the currency and limits a sharp rise in inflation. Second, people in Russia do not have the option to exchange large sums into U.S. dollars or euros. Third, companies that earn foreign currency for their services are required to convert these funds at an 80% rate. In practice, we can view today’s value of the ruble as artificially created, since it was not set by the market based on supply and demand for the currency. As for the major currency pairs in Q1: EUR/USD fell by almost 3%; EUR/GBP strengthened slightly by about 1%; EUR/JPY also rose by almost 3%; EUR/CNY weakened by around 3%; and EUR/CHF fell by more than 1.8%. Larger moves were seen in the currencies of Eastern European countries, mainly on EUR/PLN, where the pair at times strengthened by about 8%; EUR/CZK also strengthened at one point by almost 4%; and EUR/HUF by as much as 6%. These currencies later stabilized thanks to central bank interventions and also due to a decline in panic in the market, which had been triggered by the war in Ukraine. Subsequently, V4 currencies erased most of their losses against the euro.

Slovak residential real estate market

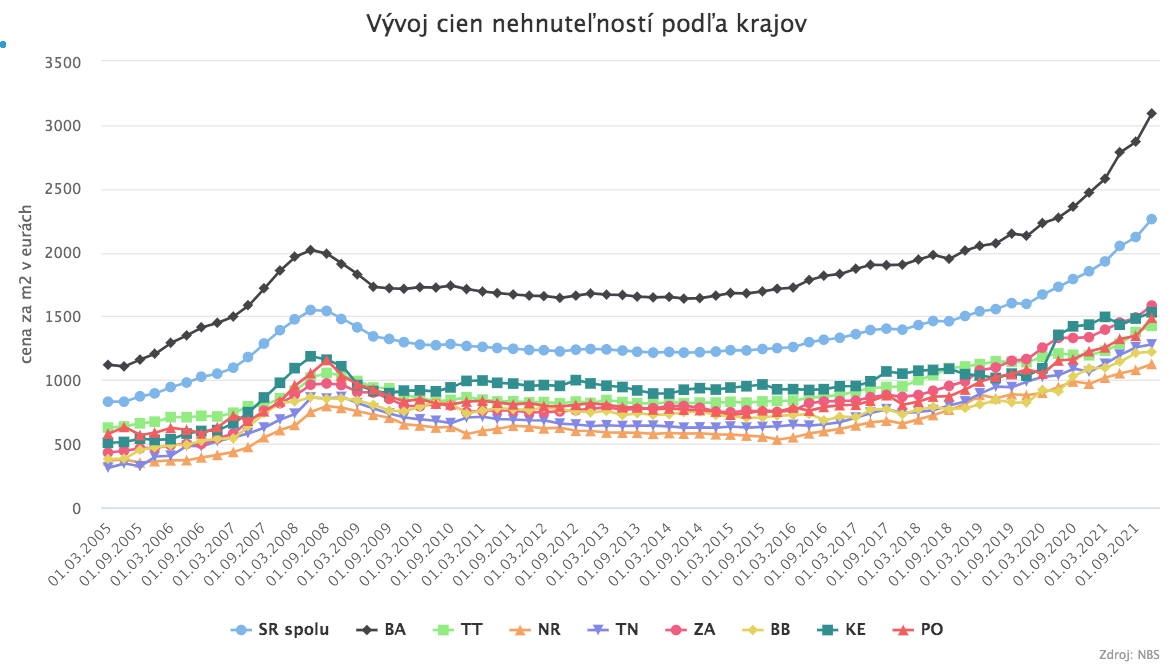

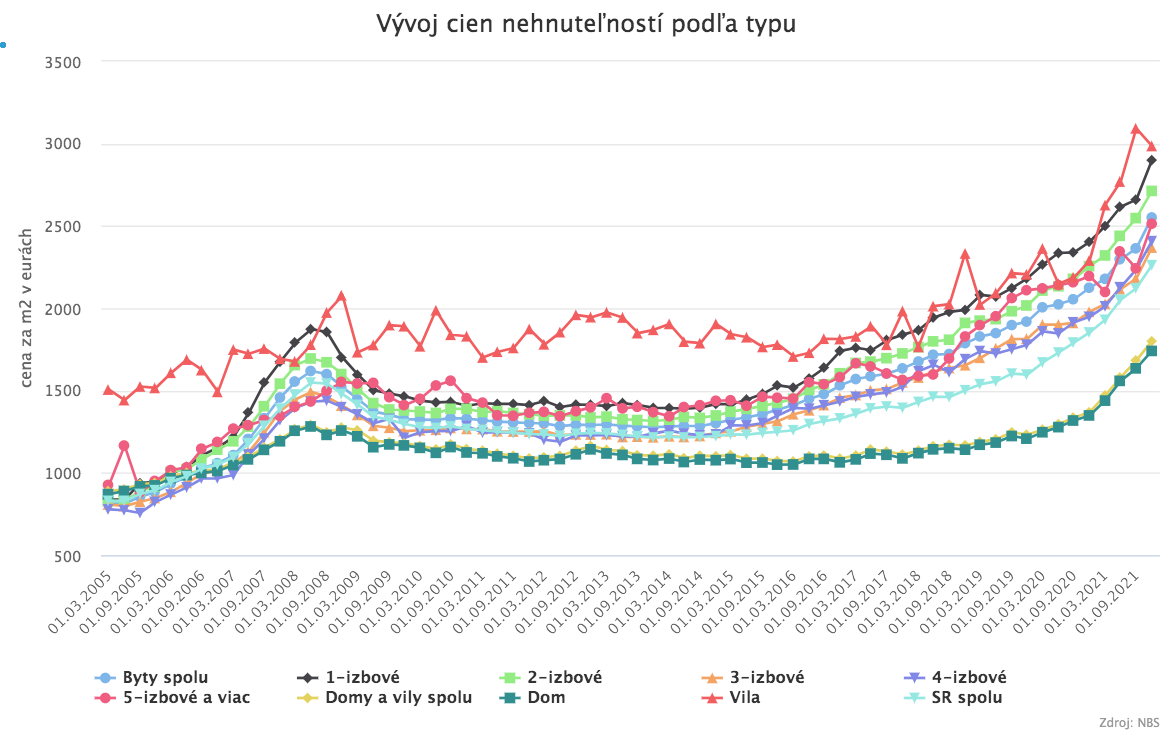

Official results for the development of property prices in the first quarter will only be available toward the end of the first half of the second quarter, but we can look at the end of 2021 and the real estate barometer. The end of 2021 was among the record periods; in Q4, property prices rose by 22.1% year-on-year, and by 18.7% for the full year. Among property categories, luxury houses (villas) rose the fastest in 2021, by 27.7% year-on-year, and among apartments, four-room apartments rose by 16.1%. The slowest-growing residential properties were five-room apartments (6.8%). Looking by region, for 2021 the clear winner was the Bratislava Region. Residential property prices there rose by 21.4%, while property in the Trnava Region increased the least (11.1%). The real estate barometer has the latest data from March 2022 and shows price growth in almost all regional capitals. In Bratislava, newer three-room apartments grew at the fastest pace (6.5%), and among older apartments, four-room apartments performed best (3.3%). The smallest gains were recorded by older three-room apartments (0.0%), and among newer apartments, four-room apartments (0.8%). Notably, a decline in prices of newer apartments in Bratislava was measured in several parts of the city. The biggest drop was in the Dúbravka district, where three-room apartments fell by 9.4%. The first declines may signal the current, or short-term, ceiling of residential real estate prices.

Current outlook for 2022

In its January forecast, the International Monetary Fund expected global economic growth of 4.4% in 2022 and 3.8% in 2023. However, this projection was already a revision of estimates from the end of 2021, lowering the growth forecast for this year by 0.5%. It is questionable how accurate the current forecast is, since it likely did not account for a war in Europe. The IMF sees inflation at 3.9% for advanced economies and 5.9% for emerging ones. The ECB also published scenarios for the coming years; for 2022 it expects inflation of 5.1% (an adverse scenario of 5.9% and a severe scenario of 7.1%). The central bank also offered an outlook for real GDP growth and expects growth of 3.7% (an adverse scenario of 2.5% and a severe scenario of 2.3%). The central bank governor opposes rapid monetary tightening to avoid stopping economic growth. Therefore, monetary tightening will be slower than in the U.S., and this year there is talk of only one increase in the key interest rate (by 0.25 percentage points). Of course, new asset purchases should be stopped, and reinvestment of existing holdings should continue. The Fed expects its economy to grow by 2.8%, revising the forecast from 4% due to the current situation in the global economy. In addition, it predicts inflation rising to 4% this year and speaks of as many as six rate hikes. It also plans to shrink its record balance sheet of around USD 9 trillion (at a pace of USD 95 billion per month). By the end of this year, we could see the key interest rate at 3%. However, the Fed is keeping its options open, and monetary policy adjustments will proceed depending on the situation. In its latest forecast, the National Bank of Slovakia (NBS) assumes, in a milder war scenario, GDP growth in 2022 of 2.8% and inflation growth of 7.6%. However, for 2023 under this scenario it expects a further increase in the price level of 9.7%, and it only sees easing inflation pressures in 2024 (2.8%). The pace of economic growth and inflation will depend on the development of the war in Eastern Europe and on energy prices, which create the strongest pressure on prices. Real estate will probably continue to rise in value in the next quarter as long as robust demand for housing can be observed. This stems from people’s fear that in the upcoming period they will not have access to the cheap financing that we have had so far.