Is pension financing well set up?

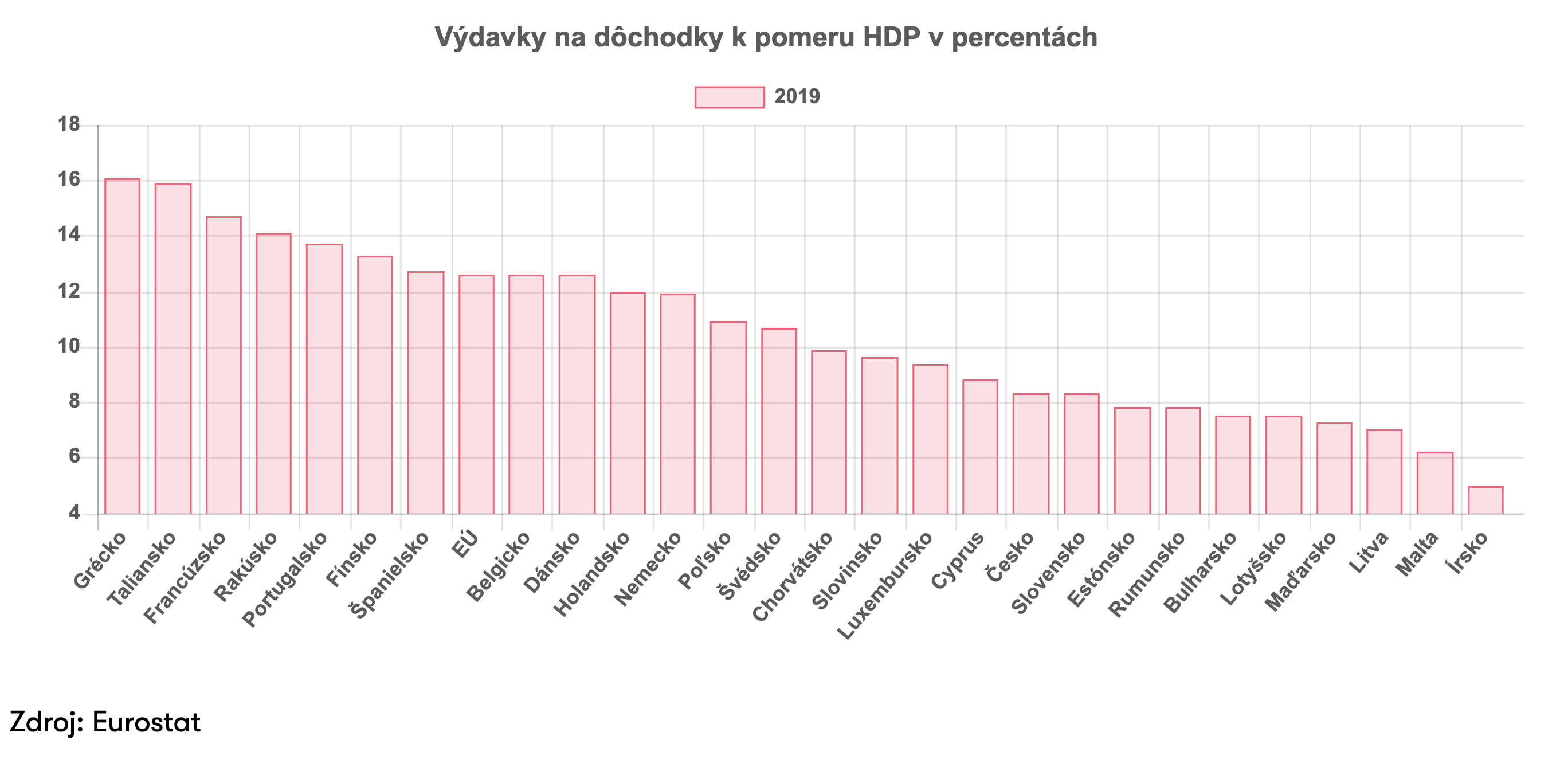

Several mistakes have been made in Slovakia’s pension system, but none appear to be irreparable so far. Most problems arise already at the stage of allocating funds across state budgets. According to the latest available data, we spend 8.3% of GDP on pensions, compared with 11.9% in Germany and 14.1% in Austria. Strikingly, highly indebted Italy spends 15.9% and Greece even 16.1%. The EU average is 12.6%. These figures indicate that Slovakia’s social system has serious shortcomings. A natural question follows: why do we allocate belowaverage funds to pensions? Do we perhaps spend more on education and healthcare than other EU countries? The answer is simple: no. We do not invest more in education and healthcare either; spending there is similarly below the EU average.

Where is the problem?

Do we have low tax and contribution burdens and therefore cannot afford pensions at EU average levels? This argument does not hold, as the average taxandcontribution burden in the EU is close to 30%, while in Slovakia it is approximately 50%. In theory we should therefore collect more revenue, but things are not so straightforward in practice. We should consider the efficiency of high taxes and contributions: do high levies encourage taxevasion? Does excessive taxation actually reduce revenue collection? In recent years Slovakia has become comparatively “successful” in terms of tax yield: revenue from taxes and contributions as a share of GDP is 37.8%, while the EU average is 35.9%. Thus, strict taxandcontribution policies do not seem to be helping Slovakia; the effect is the opposite. An aboveaverage burden of 20 percentage points has increased revenue by only 1.9 percentage points. Something is amiss. Contributions to the social insurance system and taxes are likely discouraging work.

High expenditure

Slovakia’s overall public spending is not shameful: it is slightly above average at 43.3% of GDP, compared with the EU average of 42.7%. Taken together, these data suggest that the problem lies in how money is redistributed in Slovakia. The need for reform is evident, but political will is weak because large changes are unpopular.

What is the nominal level of oldage pensions?

The average monthly oldage pension in Slovakia is EUR 515.10, which is roughly 42.5% of the average Slovak monthly wage (EUR 1,212). Average pensions vary widely across the Union: the average monthly pension in the EU is about EUR 1,030, which is roughly 54.3% of the average EU monthly wage (EUR 1,900).

We need reform

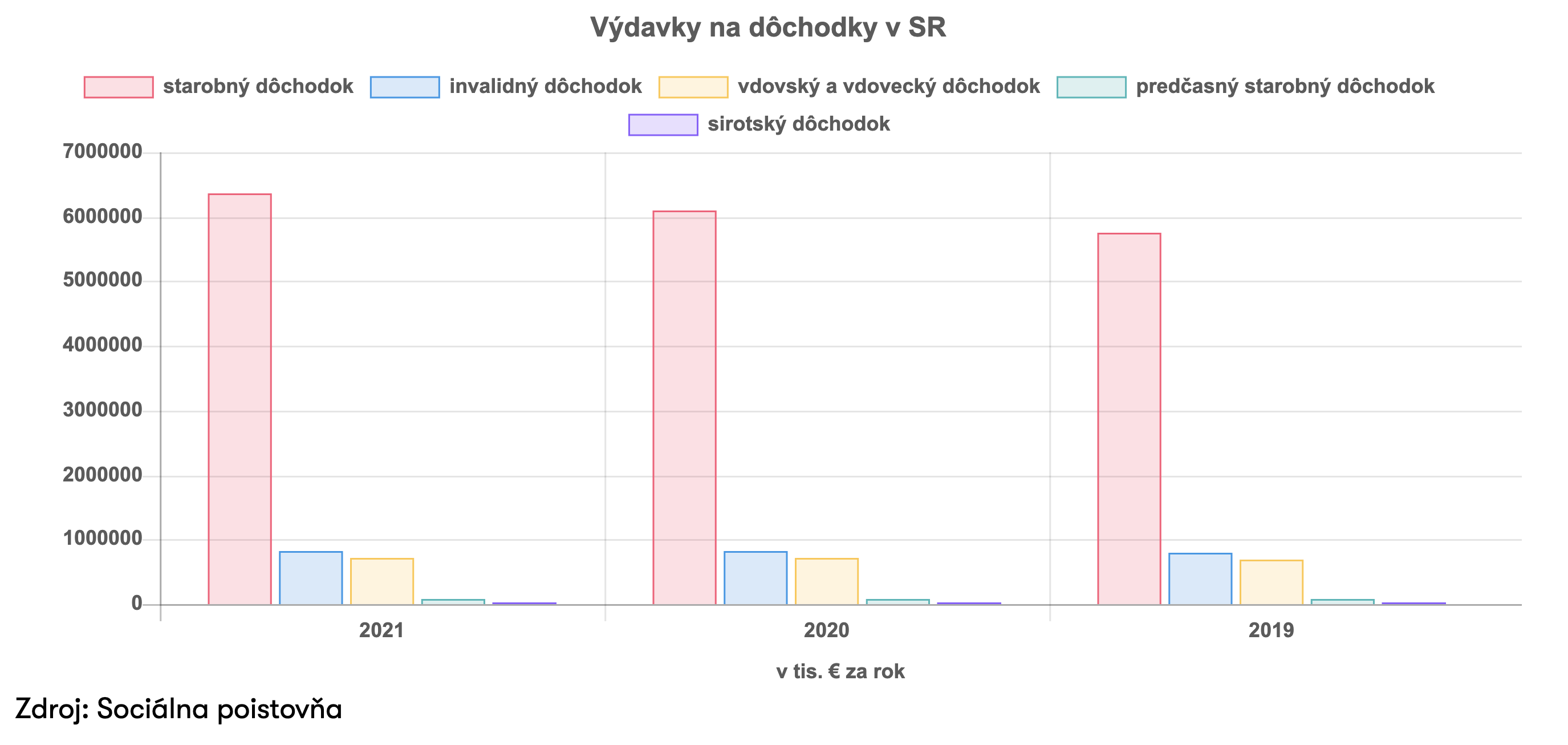

Of course, Slovakia cannot realistically expect pension levels to match those in Germany or Sweden, but the issue remains with the percentage replacement rate. This may be due to low Slovak wages (and hence low pensions), undeclared work, or a poorly designed system that requires immediate reform (including inadequate pension indexation). It is notable that in 2021 the state collected approximately EUR 8.5 billion in social contributions while the social insurance agency’s total expenditure was about EUR 9.6 billion. Under the current system, higher pensions are unlikely because the state lacks the funds to pay them. Crucially, reducing the taxandcontribution burden on labour and kickstarting the economy would, over the long term, increase state revenues and living standards. It is better to tax higher incomes at a lower rate than to tax low incomes heavily and thereby strangle the economy. A temporary deterioration in public finances might follow a reform of contributions, but over the long run lower burdens should yield a much better collection of taxes and contributions. There are many international examples of such success, and Slovakia has experienced this effect before.

Read the previous articles in the pension series: Part 1, Part 2.

Disclaimer

All texts, images, graphics and other objects placed in this document are protected by copyright and, without the prior written consent of Sympatia Financie, o.c.p., a.s., the content of this document may not be copied, distributed, modified or provided to third parties. This document contains only general information. Sympatia Financie, o.c.p., a.s. does not provide any professional advice or services via this document and accepts no liability for any damage arising directly or indirectly in connection with any person who relies on this document.