The Fed Is Not Rushing to End Monetary Stimulus

President Biden said that there was no good time to end the mission in Afghanistan and that chaos would have erupted whenever it happened. The same can be said about ending monetary stimulus. However, Fed Chair J. Powell has so far been avoiding such a step. Contrary to expectations, he did not present a specific timetable for the gradual reduction of the Fed’s asset purchases, not even at the end of last week at the (once again virtual) Jackson Hole symposium of central bankers.

Extreme monetary stimulus

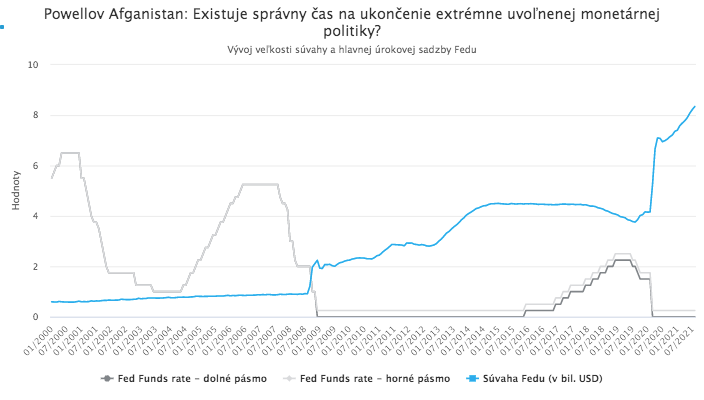

Monetary stimulus in the form of extremely low interest rates and, in particular, massive asset purchases by central banks has become a permanent feature of the economic and market environment over the past decade. The outbreak of the COVID-19 pandemic, however, led to a further expansion and multiplication of these measures. Interest rates are today, according to Bank of America research, the lowest in 5,000 years of recorded history, and central banks have spent since the outbreak of the pandemic an incredible USD 834 million every hour on asset purchases.

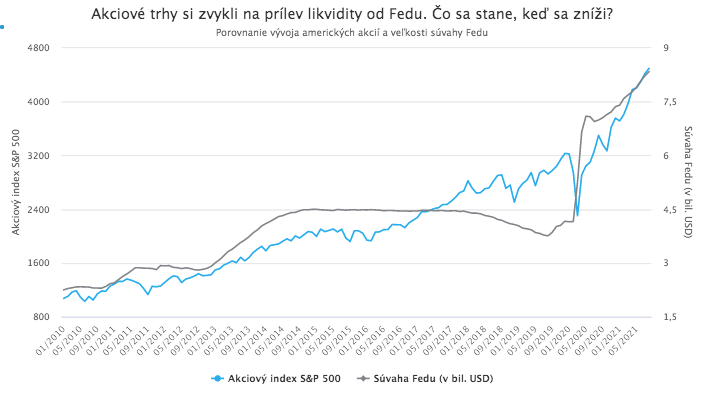

These massive monetary stimuli undoubtedly played an important role in stabilizing the economy and financial markets after the outbreak of the crisis, but they also bring many negatives, from moral hazard to a sharp increase in inequality in society (since central-bank bond purchases sharply raise the prices of financial assets, ownership of which is concentrated among the highest-income groups). They have also dramatically changed the functioning of financial markets and the behavior of investors themselves. Traditional market mechanisms have atrophied, and massive liquidity inflows from central banks have become the most important factor influencing asset prices.

It is therefore no surprise that among economists and investors, on the one hand, there is a prevailing sense that monetary stimulus should be ended as soon as circumstances allow, but on the other hand there are major concerns about what such a step would do to markets (and subsequently to the economy), and so in reality no one is particularly eager to do it. Attempts to gradually reduce stimulus through rate hikes and reductions in the volume of purchased assets were accompanied by chaos and sharp market reactions even in relatively good times before the pandemic. When the Fed, already led at the time by J. Powell, decided at the end of 2018 to continue with normalization efforts despite the raging trade war, equity markets saw their worst December since 1931, and Powell capitulated. The European and Japanese central banks, fearing the fragility of their own economies, did not even attempt normalization. Ending monetary stimulus in the middle of an economic recovery from the deep crisis caused by the COVID-19 pandemic is therefore a difficult and risky task.

Is now the right time?

However, if any of the major central banks is currently in a position to at least attempt a gradual exit from monetary stimulus, it is once again the US Fed. Its Chair hinted a few weeks ago that the Board of Governors was already discussing a plan for gradually ending asset purchases and could officially announce it later this year. The US economy began to recover from the pandemic earlier than other major economies, with the exception of China; in addition to monetary stimulus, it can also rely on strong fiscal stimulus and US equity markets (precisely thanks to central-bank support) have been rising sharply for more than a year and long since surpassed pre-pandemic levels. In the United States, moreover, inflation has begun to rise sharply in recent months, and tightening monetary policy is a central bank’s usual tool for fighting inflation. From one perspective, it thus seems that now is the right time for the Fed to begin ending stimulus.

On the other hand, concerns are also emerging as to whether now really is the right time, and whether it would not be advisable to wait a few more months. The United States is currently, like many other countries, grappling with a strong Delta-variant wave, which in several regions with lower vaccination rates has led to hospitals filling up.

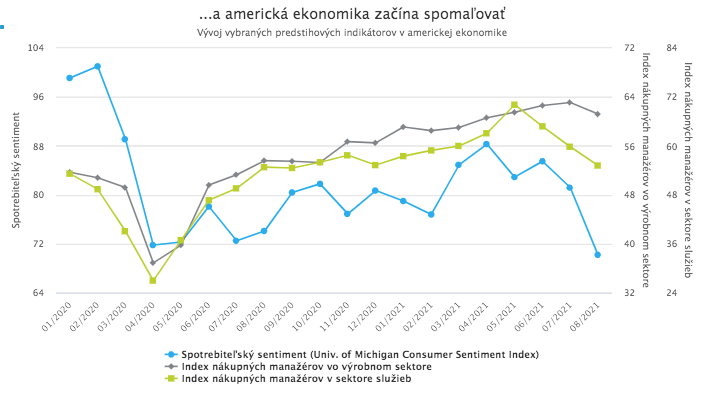

Moreover, the US economy, under the influence of concerns about the Delta variant and rising consumer prices, is already starting to show signs of slowing.

What will the exit from stimulus look like?

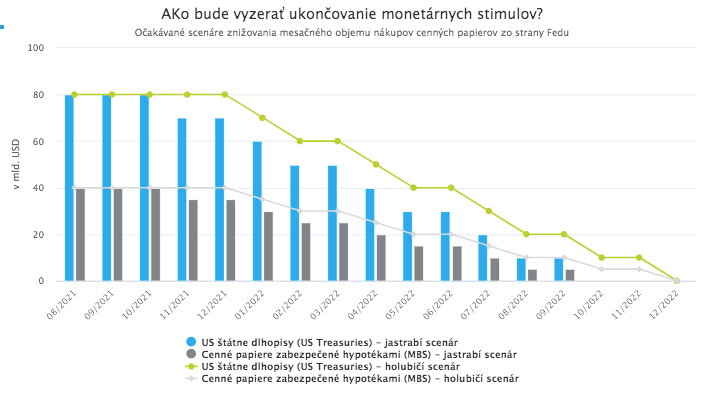

The decision to end monetary stimulus is thus difficult. There is a sense that it must be done at some point, yet at the same time concerns keep emerging about whether it is truly the right time. It is entirely possible that a “right time” does not exist in this case, because economic conditions will never be completely ideal and financial markets, “addicted” to monetary stimulus, will always react sharply to its withdrawal. At the same time, it likely holds that the longer monetary stimulus remains in place, the sharper the reaction its withdrawal will trigger. In any case, based on previous statements by J. Powell and other members of the Board of Governors, investors expect the Fed to at least announce a plan for gradually reducing the volume of asset purchases later this year. The question, however, is whether it will begin tapering already this year, and at what pace. Since the outbreak of the pandemic, the Fed has purchased securities totaling USD 4 trillion, and it is currently still buying assets worth USD 120 billion each month. USD 80 billion of this amount consists of bonds, and the remaining USD 40 billion consists of mortgage-backed securities. The most optimistic or most pessimistic (depending on one’s perspective) scenarios assumed that the Fed would begin reducing the volume of monthly asset purchases as early as November this year, and that after each FOMC meeting (there are eight per year) it would cut purchases by USD 15 billion (USD 10 billion in bonds and USD 5 billion in mortgage-backed securities).

In general, however, it is expected that if the Fed were preparing to proceed with such an ambitious plan, it would have to announce it at the September meeting (that is, one meeting before it actually starts reducing purchases) and, even before the September meeting, communicate in advance that such an announcement is coming. The Jackson Hole symposium would have been an ideal opportunity for such communication. Powell’s Friday speech was therefore watched extremely closely. Investors were looking for hints that the September meeting would bring a formal announcement about tapering asset purchases. That did not happen. Powell merely dryly repeated that the Fed could proceed with tapering later this year, but any concrete information, details, or timetable were missing. This almost certainly means that tapering will not begin already in November. It therefore seems that Powell is still weighing whether now really is the right time to end stimulus.